Four industry experts share insights

on covering these important Californians

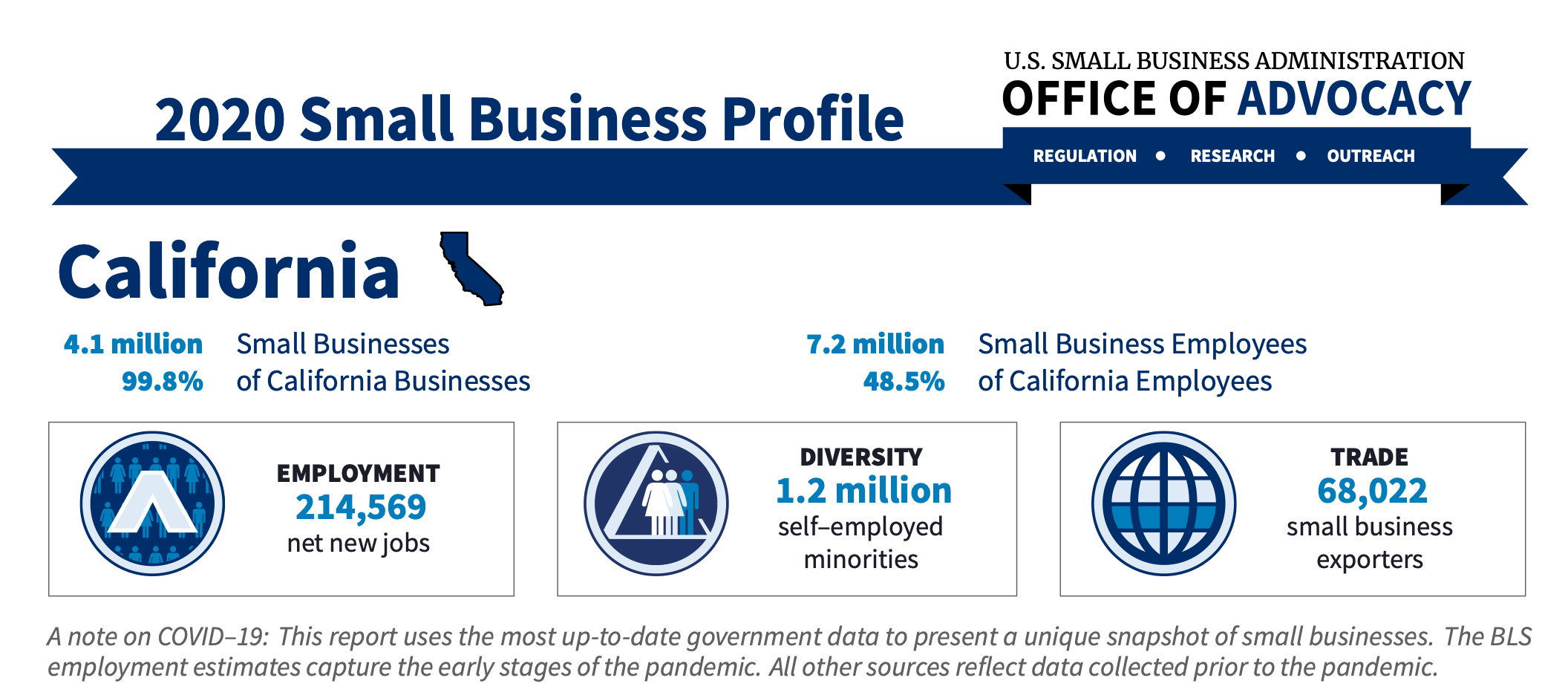

California small businesses are drivers of the state’s economic growth — creating two-thirds of new jobs and employing nearly half of all private sector employees. California is home to 4.1 million small business representing 99.8 percent of all businesses in the state and employing 7.2 million workers in California, or 48.5 percent of the state’s total workforce. From 2018 to 2022 — 5,335 new small businesses were started.

The COVID-19 pandemic has presented a significant challenge to small businesses, employers and employees. An August Small Business Majority survey found that 44% of small businesses are at risk of shutting down. Data released through the Census Current Population Survey found that minority-owned businesses are disproportionately impacted: the number of active businesses owned by African-Americans dropped by 41%, Latinx by 32%, Asians by 25%, and immigrants by 36%.

Small business support is critical to ensure these Californians are connected to the resources they need to pivot and adapt to the COVID-19 marketplace. California Governor Newsom and the legislature are using every tool at their disposal to support small businesses as they work to safely reopen and recover from this public health crisis.

THE SMALL GROUP EXPERTS

CalBroker magazine (CB): What trends are you seeing for California Small Group? Is the market growing, or shrinking? Has the pandemic caused the closure of small businesses or is it the opposite?

Dickerson Insurance Services Sales Team

With Dickerson’s digital resources, we thrived during the shutdown — and helped brokers do well as a result. Although we saw businesses close, we also saw an uptick in newly formed businesses looking for employee benefits. Many businesses that didn’t offer benefits now provide coverage to their employees. Employers are starting to hire again. People are back to work, but there’s a lot of turnover.

Grant Snyder, VP, Small Group Sales, UnitedHealthcare, California

At UnitedHealthcare, membership is holding steady with exceptional group persistency and positive attrition for in-force groups. Early in the pandemic, California certainly experienced its share of increased closures of small businesses that were centered around certain industries (such as hospitality), but that has quickly corrected itself and now we are seeing positive growth in existing groups — a good sign for the business economy.

Another trend we are anticipating is the increase in membership due to the upcoming Medicaid redeterminations. Many people will move off of the Medicaid rosters and receive coverage through their employer, which will likely increase the small group market through positive attrition.

Hadley Weiler, Regional VP, Benefits West Region, BenefitMall

The answers can vary by California regions and industries. Overall, the California market is not shrinking, but growth and hiring has slowed down as a result of California employees leaving the state for remote work, general economic downturn, and inflation when compared to pre-pandemic years. At the height of the pandemic when many small businesses were closing, many businesses that kept employees on took advantage of the Employee Retention Tax Credit (ERTC) and are still taking advantage of the ERTC, showing a rebound in California Small Groups as a whole.

The market continues to be optimistic for innovative companies in Agtech, Fintech, Healthtech, artificial intelligence, blockchain technology and ESG (environmental, social and governance) companies. Venture capital investment funding remains at one of the all-time highs for startup companies, though it has dropped significantly in comparison to 2020/2021. However, money spent on payroll and benefits are less generous due to curtailed spending.

On the other hand, the late-stage startup companies that would have gone through IPO are not seeing as fast of a growth path as they used to, partly due to lesser investment funding.

These companies are also seeing hiring freezes or even small labor force cuts. Even with an increased number of mergers and acquisitions of these late-stage startup companies, the capital/finance is pooled to scale and grow more profitably with the hiring freezes.

Another trend California brokers are seeing is assisting their clients in setting up small business sponsored group plans outside of California to accompany a shift in the workforce where companies no longer have more than 51% of employees residing in California. Startup companies are increasingly turning to remote offices and hiring as a way of saving on overhead costs.

Employers are currently struggling to afford a higher payroll to keep pace with higher inflation rates. There is a need to adjust the cost of goods to offset the overhead and payroll in the consumer products industr.This will continue to be a tight balance for employers as consumer spending decreases over the next year. This could have adverse effects on small businesses’ willingness to add to staff.

Lastly, California droughts and wildfires over the last few years have added to the struggle smaller, family-owned farms face following the pandemic. With lower crop yields and rising food costs, these farms will have to look for innovative ways to keep their doors open.

Marc McGinnis, president, Word & Brown General Agency

We continue to see growth for most brokers with whom we are working. Yes, some businesses have closed, and others have downsized, and that has certainly shaken things up for brokers and agencies. However, many brokers have seen increased opportunities because their clients’ businesses are growing. In a competitive talent marketplace, benefits can help employers differentiate themselves.

We continue to look at ways we can help brokers write more and earn more by offering a broad range of products and services backed by outstanding sales, broker resources, broker tech, compliance, and customer client experience teams.

CB: Has the pandemic increased access to ACA subsidies for small groups? Has this helped keep small groups covered?

Dickerson Insurance Services Sales Team

With the new ARPA subsidies and the impending “family glitch,” individuals and companies can take advantage of subsidies. They can keep the same benefit levels and reduce costs. We communicate this with all eligible clients, to help keep their employees happy, and save the business money.

Snyder, UnitedHealthcare

Employers definitely took advantage of available subsidies and/or loans, and those opportunities certainly made a difference in helping to keep many small businesses going. I think we’ve returned to a “new normal” scenario where businesses can focus again on growing as opposed to just surviving.

Weiler, BenefitMall

From what we have seen, the pandemic has not made much of an impact on access to ACA subsidies for small groups.

Typically, technology companies pay higher wages to attract and retain qualified employees, so these groups would not qualify for Small Business Health Care Tax credits, which are only available through the CoveredCA Small Business SHOP plan — even with the economic downturn. The California SF Bay Area minimum wage has traditionally been above the California minimum wage threshold as well, so it is very rare for these small employers to qualify.

On the other hand, small employers that do qualify may not even realize that they have health care tax credits until their certified insurance agents inform them of their eligibility. Even once informed, we sometimes see employers electing Medi-Cal (CA Medicaid) benefits instead, so they do not pay for their cost share towards the group sponsored insurance benefits.

If a small employer has already taken the tax credit for two consecutive tax years, they are no longer eligible for the Small Business Health Care Tax Credit. Therefore, this is not a long-term solution for small groups.

McGinnis, Word & Brown

Affordable Care Act (ACA) subsidies are available only to individuals and families who purchase coverage through a public exchange, so they have minimal effect on small businesses. If an employer does not offer group coverage and, instead, steers workers to the exchange to purchase coverage on their own, some employees could benefit from expanded subsidies. What really helps groups shop for the best value on group health and other coverage is working with a broker who can thoroughly shop the market.

Our proprietary quoting technology delivers side-by-side comparisons with highlighted plan differences. Our provider and Rx searches ensure clients get access to their preferred providers in the plans they’re considering. A benefit for employers in providing employee benefits is the ability to reduce taxes and take a tax deduction for the expense.

CB: How has inflation affected small businesses in terms of keeping workers insured? Do you have special offerings to help? Are you seeing adjustments in benefits packages?

Another trend we are anticipating is the increase in membership due to the upcoming Medicaid redeterminations. Many people will move off of the Medicaid rosters and receive coverage through their employer, which will likely increase the small group market through positive attrition.

— Grant Snyder, VP, Small Group Sales, UnitedHealthcare, California

Dickerson Insurance Services Team

Employers are looking for ways to cut insurance costs. Most employers will offer to pay 50% of the lowest cost, high deductible plan and shift the responsibility to the workers. More employers are looking into alternative funding to help lower their costs.

Businesses are also looking for cost-effective measures to keep their doors open. Dickerson and our broker partners are continuing to provide lower-cost core benefit solutions coupled with ancillary benefits to supplement the out-of-pocket costs of the employees. These in-depth strategy discussions allow us to create a packaged solution that benefits the employee and the employer’s overall bottom line.

Snyder, UnitedHealthcare

Inflation is real and has a significant impact on everything we do. To date, we have not seen a huge increase in benefit buy-downs. We all know when small businesses have to pay more for goods and services, the ripple effect is higher prices for the end user and less consumer spending on discretionary items. We’ve found innovative ways to support our clients and members.

For instance, we partner with organizations like Peloton to help more people get or stay active and improve their overall well-being. As part of their health benefits, as many as 10 million UnitedHealthcare commercial members may be eligible for a yearlong subscription to the Peloton App membership — or a three-month waiver toward a Peloton All-Access membership – at no additional cost. Eligible UnitedHealthcare members in most states receive preferred pricing on select Peloton connected fitness products, including the Peloton Bike, Bike+ and Tread.

This summer UnitedHealthcare announced an important step in its continued efforts to make prescription drugs more affordable for people. We eliminated out-of-pocket costs for preferred short- and long-acting insulins, as well as the following preferred emergency use drugs that are critical in acute, life-saving circumstances.

These include medications for severe allergic reactions (epinephrine), critically low blood sugar (glucagon), opioid overdoses (naloxone), and acute asthma attacks (albuterol). As early as Jan. 1, 2023, this will become a standard offering available to UnitedHealthcare fully insured clients with OptumRx new business plans and for existing plans upon renewal date.

Weiler, BenefitMall

Generally speaking, at the national level, inflation has affected small businesses because to keep cost down, businesses have reduced contribution levels. So in order to have a strong benefits package, employers are pursuing more specialty/non-medical strategies and offering voluntary products like worksite, legal, pet and additional HSA/HDHP plan offerings.

That said, we do not expect California small employers to make major plan or contribution strategy changes in Q4 2022/Q1 2023. California small group carriers filed their rates in May 2022, right before inflation hit, so Q4 medical renewals are still in single digits or low double digits.

Q1 medical renewals are expected to be slightly higher, but not significant enough for small employers to make significant plan changes. Employers are also reluctant to reduce company-sponsored plans and contributions this year since it could cause employee dissatisfaction as their workload increases in light of hiring freezes or small labor force cuts.

Small employers may consider downgrading the benefits at next year’s renewal if health insurance premiums continue to rise, or implementing level funding or HRA strategies to help curb employer costs. BenefitMall partners with a number of carriers that have level funding offerings for small employers in California. Typically, this is a strategy for 25+ life groups where employers with good risk scores could see potential savings by using level funding plans.

Small startup companies that receive investment funding will continue with fully insured strategies, but employers are more prudent with their employee benefits spending these days. For example, we are seeing small employers electing Gold/Silver tier plans as base coverage instead of Platinum/Gold plans. Small group HMO or narrow HMO networks will continue to serve as cost saving solutions as employers look to offer rich benefits at a lower premium.

There is also an increased employer interest in offering employee assistance programs (EAP) and mental health wellness packages, which have become a hot topic during the pandemic. As inflation continues to impact the day-to-day lives of employees however, brokers are seeing more inquiries from small employers that want to purchase enhanced mental health/wellness benefits to assist their employees.

In addition to virtual behavioral health services, some small group medical carriers are offering free employee assistance to medical members, while others partner with apps like Ginger or Talkspace to offer additional mental health wellness support as value-add services to small group employees.

Small businesses are also more willing to look at alternative funding solutions. While ICHRAs can be a solution for some small employers looking to save premium, we’re not seeing huge traction in the California market since the indivi-dual health medical carriers do not offer broad network plan options. For small employers that are looking to attract and retain employees, this is not a popular solution since it is more difficult to administer versus a small group employer sponsored plan.

“Brokers are taking a more consultative approach in helping small employers now. To be successful, brokers need to know what additional products can keep the group’s benefits package robust, while keeping contributions manageable. They need to be more comprehensive with their benefit solutions and look to offer other lines either by partnership or acquisition. … Brokers must also be willing to do their due diligence and embrace technology.”

— Hadley Weiler, Regional VP, Benefits West Region, BenefitMall

McGinnis, Word & Brown

Businesses are seeing higher premium increases than in the past few years. The pandemic reduced costs for insurers as utilization was lower. Now, utilization is up as individuals and families catch up on some of the medical care postponed during the past two years. Employees are looking for different benefits today. In response, employers are expanding offerings, giving employees more of a say in their benefits. It’s not really driven by inflation, but by changing needs and demands from employees. Our approach is – and always has been – to work

As shown in the chart, six health insurance companies accounted for 96% of the enrollment in small group health insurance plans in California. Source: Healthcare.com

with brokers to help them find the right balance to satisfy employees’ needs and wants, while still helping employers control their costs.

CB: What are the keys to being a successful broker to small groups right now?

Dickerson Insurance Services Sales Team

Go above and beyond and bring something new to the table other than the traditional HMO/PPO plans. Offer other lines of coverage such as ancillary products. Stay in contact with your clients often. Communication, collaboration and accountability are key!

Being able to offer everything to a client is crucial. Dickerson has the right connections and contracts to do that. We communicate strategies effectively with the client, make good on promises, and ensure that we administer the client’s accounts diligently.

Snyder, UnitedHealthcare

My most candid advice is to stay close to your customers as they need you more than ever. Don’t be afraid to share new product offerings, such as level funding, which can reduce overall premiums for small businesses with little downside risk. Do your homework in order to recognize and communicate the nuances between plans and the differences between carriers.

Weiler, BenefitMall

Brokers are taking a more consultative approach in helping small employers now. To be successful, brokers need to know what additional products can keep the group’s benefits package robust, while keeping contributions manageable.

They need to be more comprehensive with their benefit solutions and look to offer other lines either by partnership or acquisition, such as property and casualty and workers compensation. The successful ones have partnerships with benefit administration technology, payroll, human resources, and compliance services so they can be a simple one-stop shop solution for employer groups.

Brokers must also be willing to do their due diligence and embrace technology. Know how to market your group, understand their current needs, look at all avenues of insurance from traditional, self and partial funding, etc. in this post-pandemic, remote work environment. Brokers must also be knowledgeable with carrier underwriting guidelines, contribution strategies, alternate funding solutions and compliance.

Due to the Consolidated Appropriations Act, transparency in broker commissions also requires the successful broker to provide additional value-add services such as onboarding/offboarding tools and benefits booklets and enrollment videos to win agent of record and retain clients.

McGinnis, Word & Brown

A broad portfolio and service are key. Employers are expecting more from their benefits brokers, and it is important brokers have a reliable partner to help them address changing needs and ease their administrative burden. That includes offering products from multiple carriers, quoting and enrollment assistance, online forms and marketing tools, HR and benefits support for clients, answering compliance-related questions, and delivering value-added services clients will appreciate. As California’s leading independent general agency, we’ve been partnering with brokers for decades to help them be more successful.

CB: What does the future look like for small group health?

Dickerson Insurance Services Sales Team

We’re seeing a shift to more remote positions. The location of the employee, in many cases, is irrelevant. Companies have employees scattered across the country, so the future of small group health will revolve around more creative benefit offerings that can accommodate the entirety of the workforce. Dickerson’s prepared for these changes, as we’ve been creating solutions like this for years.

Snyder, UnitedHealthcare

For UnitedHealthcare in California, small group health is a focus — it’s what we do and we do it well. We see a huge upside for our health plan in continuing our commitment to small business, and our partnership with our clients to provide improved operational efficiencies, a wide variety of product offerings, and exceptional service for our members. Our mission is to help people live healthier lives and make the healthcare system work better for everyone.

UnitedHealthcare is not just a local state-based plan; it has the strength of a Fortune 5 enterprise connected across all aspects of the healthcare delivery system and ready to help transform it. We’re exceptionally positioned to pivot and change, as needed, and are ready to help small businesses in California flourish.

Weiler, BenefitMall

The future is bright for small group health. This is not the first time brokers have had to weather economic downturns, and with economic changes come opportunities. Employee benefits will continue to play an essential role for small businesses as they seek to hire and retain quality staff, regardless of industries. The challenge will be in expanding benefits packages without increasing contributions for employers. Small group health is strong, but agent competition is fierce, especially with broker acquisition. We see plenty of opportunities for small brokers and mid-level shops.

On the startup front, venture capital firms continue to search for their next unicorn. U.S. and foreign investors are still cautiously optimistic about the next great innovation.

However, we may not see as many startups in California compared to other states, as they can offer attractive business tax incentives, while the cost of living in California continues to increase — it’s becoming more expensive for employers to operate their small business in the state.

Overall, the future outlook is optimistic, but brokers will have to design benefits packages that include emotional and financial wellness to support both small business employers and employees while keeping the health care costs affordable and attractive.

There are increasingly competitive, unique funding offerings available in the marketplace, as well as investments in technology to fuel speed, growth and trusted data integrity. The key for many brokers will be to work with a trusted General Agency partner to offer robust benefits offerings, backed by digital enrollment and benefits administration, in order to take advantage of near-term and long-term growth opportunities.

McGinnis, Word & Brown

We believe the future is bright for Small Group Health and for brokers. California has more than 4.1 million small businesses that represent more than 99% of all businesses in the state. Small businesses drive nearly half (48.5%) of the private workforce in the state, and they have been a driving force in America’s recovery from COVID-19.

The Census Bureau says net job growth is strongest among businesses with fewer than 20 employees. The past two years have been challenging, but according to a recent survey, fewer than a quarter of small businesses furloughed or laid-off employees. We continue to grow, and we are committed to helping brokers adapt and grow their businesses as we all work to address the changing needs of employers and employees.