This article starts off where Part 1 left off in the March, 2021 issue.

BY DOROTHY COCIU WITH MARILYN MONAHAN

SOMETHING NEW – ACA CHANGES, TIC AND CAA

– ACA New Item Summary

I mentioned something new above related to the ACA: The loss of the Good Faith Penalty Relief. In addition, there have also been changes to Form 1095-C, including new indicator codes, which were designed primarily for individual coverage health reimbursement arrangements (ICHRA). There is also a rule pending on the extension of time to distribute forms, and a proposed rule pending on the threshold for electronic filing. The majority of the “new” items, however, are related to the Transparency in Coverage rules and the Consolidated Appropriations Act (CAA), including the No Surprises Act and Broker Compensation Disclosure requirements beginning in 2021.

TRANSPARENCY IN COVERAGE (TiC)

I have previously written detailed articles on the TiC that were published in Cal Broker:

– Feb.2021: https://www.calbrokermag.com/in-this-issue/transparency-in-coverage-rules/

– Oct. 2021: CAA, Part 1: https://issuu.com/californiabrokermagazine/docs/calbroker_oct_2021_issue,

– Dec. 2021: Part 2, https://www.calbrokermag.com/in-this-issue/caas-no-surprises-act-part-2/

You can refer to those articles for more information. In summary, for the purpose of this Compliance for 2022 article, I will summarize the important items.

The Transparency in Coverage rule is actually tied in with the Affordable Care Act (ACA), as the ACA did call for transparency in healthcare coverage, in addition to the CAA rules. The Transparency in Coverage final rule was issued November 12, 2020. The CAA, signed December 27, 2020, includes the “No Surprises Act,” which is from Title I of Div. BB, and “Transparency,” from Title II of Div. BB. There were later FAQs Part 49, which were issued on August 20, 2021. These FAQs included new effective dates for some, but not all of the TiC and CAA provisions. I’ll try to simplify and summarize for you, and include the ”To Do” items for health plans.

THE ACA: TRANSPARENCY IN COVERAGE

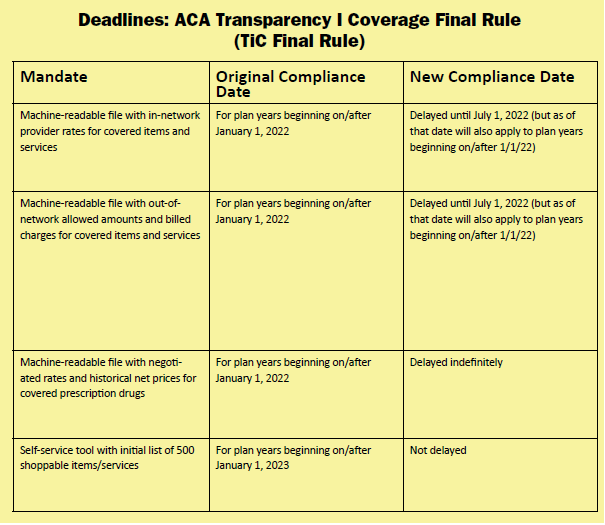

There were two parts to the TiC final rule; public disclosure and online service tools. Originally, for plan years beginning on or after Jan. 1, 2022, plans/issuers (except grandfathered plans) must make public three machine-readable files that will include detailed pricing information that would show the following:

1. In-network provider rates for covered items and services

2. Out-of-network allowed amounts and billed charges for covered items and services

3. Negotiated rates and historical net prices for covered prescription drugs

The new compliance deadlines for the above items are as follows, according to FAQs Part 49:

• Delayed until July 1, 2022, but also applies to plan years beginning on or after 1/1/22

• Delayed until July 1, 2022, but also applies to plan years beginning on or after 1/1/22

• Delayed indefinitely, because of potential overlay with CAA provision on pharmacy benefits Under the ACA’s transparency in coverage provisions, an online self-service tool for plans and issuers (except grandfathered plans) must make available to participants personalized out-of-pocket cost information, and the underlying negotiated rates, for all covered health care items and services. This includes prescription drugs, through an internet-based self-service tool, and providing a paper copy form upon request. The initial list of 500 shoppable services or items identified by the departments to disclose must be available for plan years on or after January 1, 2023. All other items and services must be made available on or after January 1, 2024.

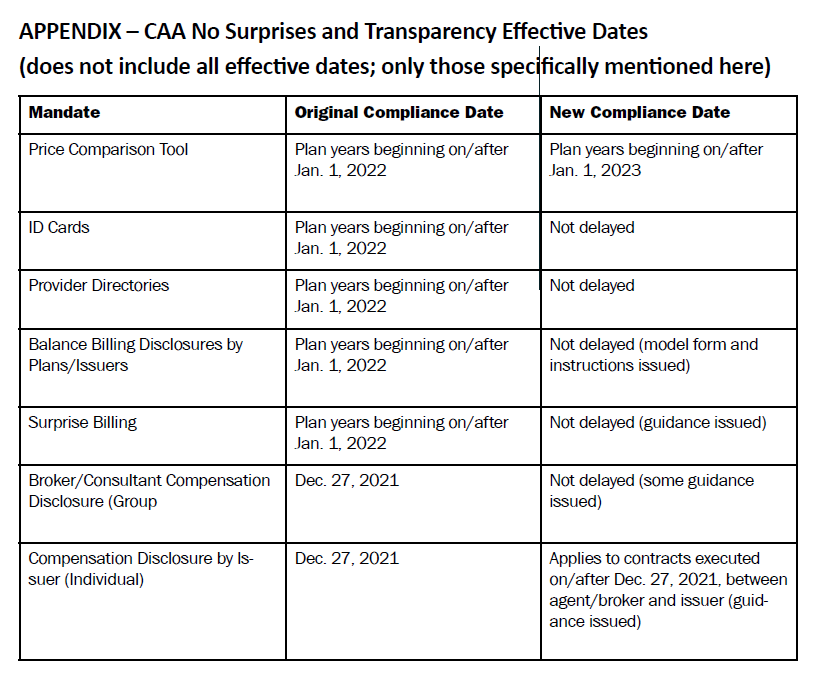

Incidentally, the CAA price comparison tool is “largely duplicative” of TiC, but also applies to grandfathered plans, and includes a requirement to provide information over the phone. It was delayed until January 1, 2023.

Plan sponsors with fully insured plans don’t need to do a lot of extra work here, as their carriers will be doing the transparency work. However, they are required to enter into a written agreement with the carrier or issuer. I’m not sure how that will work at this time, as to whether this is something the carrier will automatically provide or if the plan sponsor employer will need to create an agreement of some sort. I’m sure we’ll have more guidance in the future.

Self-funded plans must either comply themselves or outsource through a written agreement. As someone who works with a lot of self-funded plans, I can’t see any self-funded plans doing this themselves; they will need to rely on their TPAs or other vendors (such as a PBM for the prescription portion, a PPO network or Reference Based Pricing vendor) to do this on their behalf, which means that they will need a written agreement for each of those vendors. The plan sponsor will remain liable, which could be very worrisome for the plan sponsor employers.

HOSPITAL TRANSPARENCY

Hospital transparency was a part of the ACA. Regulations required hospitals to publicly post a machine-readable file containing a list of all standard charges for all items and services, and a consumer-friendly list of standard charges for 300 “shoppable” services, by Jan. 1, 2021. As most of us have likely noticed, many hospitals to date, over a year after the effective date, have not complied. In response to the non-compliance, on Aug. 4, 2021, CMS issued a proposed rule that would make several changes to the hospital price transparency regulations, including an increase in penalties. If adopted, the new penalties would be in effect as of Jan. 1, 2022. That has now passed, so we’ll see if hospitals actually comply. The good news for employers is that they have no action items for hospital transparency. (As a broker, however, I would point out to employees in open enrollment meetings that this is in effect, and perhaps encourage plan participants to seek out hospitals that are complying.)

CAA “NO SURPRISES ACT” AND

“TRANSPARENCY” DEADLINES & EMPLOYER REQUIREMENTS

The chart for the original and new compliance date for all of the No Surprises Act and Transparency is quite lengthy, so I’ll include that in an appendix below. For the purpose of informing readers, I will include in this article the relevant items for employer plan sponsors.

NO SURPRISES ACT REQUIRED ID CARD ITEMS

Employers must issue new ID cards to plan participants with required new No Surprises Act items, which include the following new items:

• The annual deductible in-network

• The annual deductible out-of-network

• The annual out-of-pocket max in network

• The annual out-of-pocket max out of network

• Contact phone numbers for assistance to the participants for all parts of the plan (claims, utilization review/pre-certification, etc.)

• A website and helpful, descriptive information on how to find network providers

PROVIDER DIRECTORIES

Provider directories also have new requirements due to the CAA. Provider directories require a verification process to be assured providers listed are current, a response protocol to timely respond to inquiries, a public website or database and mandatory disclosures. In the event of network directory errors, the plan or issuer cannot require participants to pay more than the network rate, and all amounts must count toward the participants’ deductible or out-of-pocket limit.

The directories must also include a mandatory disclosure in a printed directory.

There is a helpful FAQ (Number 49) that is available from CMS at: https://www.cms.gov/CCIIO/Resources/Fact-Sheets-and-FAQs/Downloads/FAQs-Part-49.pdf

To summarize the To-Dos for plan sponsors, they should be sure to comply with the ERISA and ACA requirements (old), the CAA and TiC rules (new), and understand how the No Surprises Act and CAA will change the marketplace to a certain extent.

GRANDFATHERED PLANS

It was at first a relief for grandfathered plans when they learned that grandfathered plans are not subject to certain provisions in the ACA. For example: preventive care, the TiC rule, patient protections regarding the choice of providers and emergency services. But the CAA had another idea for grandfathered health plans. Grandfathered health plans ARE subject to the CAA (see FAQ 11). Specifically, the Surprise Billing interim final rule (IFR) states that the patient protection rules from the ACA now apply to grandfathered plans — meaning that grandfathered plans must add a patient protection notice to their plan documents. The IFR also states and rewrote rules on emergency services, which now also apply to grandfathered plans.

Under the TiC rules, the prescription drug reporting requirement does not apply to grandfathered plans, but a similar requirement in the CAA does. The departments have delayed the enforcement of the TiC rule and are working on updated rulemaking to address these overlapping requirements. The self-service tool requirement in the TiC rule does not apply to grandfathered plans, but similar price comparison tool language in the CAA does apply. So, bye-bye grandfathered plan exemptions. As they did in the prescription reporting requirement, the departments are delaying enforcement of the CAA, but not the TiC rules, and are working on updated rulemaking to address the overlapping requirements.

CAA – THE NO SURPRISES ACT: SURPRISE BILLING

I’ve written and Cal Broker has published detailed articles of mine on the No Surprises Act, which can be found in the October and December issues, 2021, as referenced with hyperlinks (online) earlier, so I won’t get into a lot of details here for this article. I will summarize the important items for plan sponsors.

As a bit of background, most health plans, whether group, individual, Marketplace or Medicare plans, offer a network of providers and facilities (PPO or EPO network) that agree to accept payment of an established, contracted rate. Non-network providers, however, generally charge higher amounts as there is no contracted pre-established rate. In many cases, out-of-network providers may balance-bill the patient for the difference between the billed charge and the amount the health plan or insurance has paid, unless prohibited by state law. It’s important to note, however, that balance bills can happen in both emergency and non-emergency care.

In an emergency situation, the patient generally goes to the nearest emergency room. That’s what we all want them to do. Even if the ER happens to be a contracted PPO facility, not all of the providers working inside the ER may be contracted under their network. This often results in balance billing (charging the difference between the billed amount and the amount the plan pays). I’ve historically used the term “Forced Providers” in these scenarios. Common examples of these providers include ER physicians, anesthesiologists, pathology/lab/x-ray, rehabilitative care, physical therapy, neonatology, surgeons, and assistant surgeons. It would be easier if patients were trained to ask those providers “who pays you?” If that were to happen, many surprise bills may not occur, as they would know they are not contracted providers. Unfortunately, that rarely happens.

We often see surprise bills in Air Ambulance billings. I’ve seen air ambulance charges in the 6-figure area on numerous occasions. Sometimes this happens even when they are air lifting from a resort or remote community to the nearest hospital or trauma center just 40 miles or less away. In most cases, surprise medical bills usually DO NOT count toward your deductibles or OOP Maximums. That is something that plan participants should also be trained on, yet little of this occurs.

The Interim Final Rules apply to group health plans and health insurance issuers offering group or individual coverage, including grandfathered health plans, effective Jan. 1, 2022. So yes, this is in effect now for many health plans. They do not apply to retiree-only plans, excepted benefits, short term limited duration plans, HRAs, FSAs, or HSAs.

The provisions of CAA’s No Surprises Act related to surprise billing are quite comprehensive. In summary, Part 1 of the IFRs banned surprise billing for emergency services. Emergency services, regardless of where they are provided, must be provided on an in-network basis without prior authorization. The rules also ban high out-of-network cost sharing for emergency and non-emergency services. In addition, patient cost sharing (such as coinsurance or deductible) cannot be higher than if such services were provided by an in-network doctor, and any coinsurance or deductible must be based on in-network rates. The No Surprises Act also bans out-of-network charges for ancillary care (like an anesthesiologist or assistant surgeon) at an in-network facility in all circumstances and bans other out-of-network charges without advance notice. Providers and facilities must provide patients with a plain-language consumer notice explaining that patient consent is required to receive care on an out-of-network basis before the provider can bill at the higher out-of-network rate.

What does this mean for plan sponsor employers? They will need to meet with their brokers and consultants, as well as their insurers or TPAs and prepare notices and amend plan terms, as necessary.

It’s important to note that state rules continue to apply for Balance Billing protections. Here in California, we have balance billing laws for fully insured plans, but none for self-funded plans.

ADMINISTRATIVE CONCERNS WITH NO SURPRISES ACT

The No Surprises Act throws confusion into the claims payment industry by requiring that coverage be provided without limiting what constitutes an emergency medical condition, solely on the basis of diagnosis codes, such as the ICD-10 codes. The federal departments appear to have expressed their disapproval of claims practices which do not look at all of the facts and circumstances, relying solely on the diagnosis codes to determine if a claim is eligible for payment. Many plans and claims administrative practices will automatically deny an emergency claim, for example, based on a predetermined list of final diagnosis codes, without regards to the actual symptoms being presented to them at the time of care. It is often only following claim denial that a plan or claims administrator will review all of the facts, and generally upon a formal (but sometimes informal) appeal.

A medical condition manifesting itself by acute symptoms of sufficient severity (including severe pain) such that a prudent layperson, who possesses

an average knowledge of health and medicine could reasonably expect to:

- place their health in serious jeopardy

- seriously impair bodily functions, or

- cause serious dysfunction to a bodily organ or part

Plans must ultimately determine whether the standard was met by reviewing presenting symptoms, without imposing any type of time limit between onset and presentation for emergency care. These provisions may require Plan Amendments. Plan sponsor employers should also look to their TPAs if self-funded, and check their next Evidence of Coverage document from their fully insured carrier, to see if the claims processes have been updated. Self-funded employers should also check with their TPA to see that their internal training manuals have been updated.

NO SURPRISES ACT NOTICE

Besides ID cards and provider directories, Plan Sponsors are also required to put out a No Surprises Act Notice to all plan participants, effective with their renewal dates on or after Jan, 1, 2022. A model notice was provided at: https://www.cms.gov/files/document/model-disclosure-notice-patient-protections-against-surprise-billing-providers-facilities-health.pdf.

SOMETHING CHALLENGING

The QPA and Independent Dispute Resolution Process of the No Surprises Act: Qualified Payment Amount (QPA) & Independent Dispute Resolution Process (IDR)

Again, I’ve written detailed articles on the QPA and Independent Dispute Resolution Process of the CAA (see CalBroker Dec. 2021, noted earlier), but I do want to summarize for this article. I will say that these two new terms and processes will definitely be challenging for those involved in the process of making determinations, and there will be a very long learning curve before these become easy, every-day terms and administrative tasks.

The QPA is the median of the in-network (or contracted) rate in a geographic area. It also applies in other portions of the law, including the base-line factor that an arbiter may consider when they determine the final amount to be paid under the new federally-established independent dispute resolution process.

Under the No Surprises Act, when a self-funded plan and an out-of-network provider cannot agree on a rate, they must go through an independent dispute resolution process (IDR).

A median contract rate should be determined by taking into account every group health plan offered by the self-insured plan sponsor. The IFR allows for administrative simplicity for self-funded plans to permit the TPA who processes their claims to determine the QPA for the plan sponsor by calculating the median contract rate based on all of the plans that it processes and administers claims for. The IFR states that the contracted rates between providers and the network provider for the health plan would be treated as the self-insured plan’s contracted rates for purposes of calculating the QPA.

THE INDEPENDENT DISPUTE RESOLUTION PROCESS

If a payer, such as a carrier or health plan, cannot resolve a payment settlement with a provider, then the payer and provider must resolve the payment dispute using methods of negotiation and arbitration. Plans and providers may use only a Certified Independent Dispute Resolution Entity (I have adopted a previously stated new acronym that I heard first from the Self-Insurance Institute of America the CIDRE).

The No Surprises Act requires payers to send an initial payment or denial of payment of a claim no longer than 30 days after a claim is submitted. After the 30-day period, either party may begin negotiations on a claim. If the parties involved cannot agree on payment terms during the 30-day period, then they will move to an Independent Dispute Resolution (IDR) process. This process may be initiated within 4 days of the 30-day period (for a 34-day window).

Each entity will offer a final payment amount and then the arbiter will use a variety of factors to determine the final amount, including geographic areas, service codes, etc. The intent is to make it fair to both parties. Under the IDR process, they are not allowed to use lower payment rates such as Medicare or Medicaid (however, self-funded plans using Reference Based Pricing will be able to use a variation of Medicare rates, as I describe below).

The IDR does not impact the consumer or plan participant. The dispute is between the provider and the health plan. The provider has no recourse against the consumer, and therefore, it is not an adverse benefit determination.

CMS created a federal portal website where providers and plans will submit their payment disputes, which can be found at: https://www.cms.gov/nosurprises/consumer-protections/Payment-disagreements.

The full website contents can be found at: https://www.cms.gov/nosurprises. Included in that portal is an application process for entities to become a certified independent dispute resolution entity, or an arbiter for the process. Before initiating the federal independent dispute resolution process, disputing parties, according to CMS, must initiate a 30-day “open negotiation” period to determine a payment rate. In the case of a failed open negotiation period, either party may initiate the federal independent dispute resolution process. The parties may then jointly select a certified independent dispute entity (or CIDRE) to resolve the dispute. The CIDRE and personnel of the entity assigned to the case must attest that they have no conflicts of interest with either party. If the parties cannot jointly select a CIDRE or if the CIDRE has a conflict of interest, the federal departments will select a CIDRE for them.

After a CIDRE is selected, the parties will submit their offers for payment, along with supporting documentation, into the federal portal. The CIDRE will then issue a binding determination selecting one of the parties’ offers

as the out of network (OON) payment amount. Both parties must pay an administrative fee ($50 each for 2022), and the non-prevailing party is responsible for the CIDRE entity fee for the use in this process.

When choosing an arbiter, there can be no conflicts of interest on either side. The arbiter cannot be an employee or former employee of a disputing party within the past year or a former employee of the federal government within a year of the time which the employee left the employment of the government.

They cannot have a financial, professional, or family relationship with either party. In addition, the arbiter cannot be owned, either directly or indirectly, by an insurance carrier or medical provider. The arbiter also cannot be an affiliate/subsidiary of a professional trade association for the group health plan, carrier, or providers.

The arbiter needs to have sufficient expertise in the arbitration and claims administration of health care services, managed care, billing, coding, medical and the law. They must also have expertise which is considered sufficient in the field of medicine, especially where the payment determination depends on the patient acuity or the complexity of the medical procedure, or the level of training, expertise, experience and quality and outcome measurements of the provider or facility that furnished the medical service or services. Arbiters are required to maintain current accreditation from a nationally recognized and relevant accreditation organization, such as the Utilization Review Accreditation Commission (URAC), or employees must have requisite arbitration and topical training.

So, the bottom line is, not everyone can apply and be accepted as a CIDRE (also, the payment they receive is predetermined and not overly lucrative, so I don’t see thousands of CIDRES stepping up to apply).

When submitting “offers” of payment, both parties must submit an “offer” for the OON payment in dollars and a percentage of the QPA represented by that dollar amount, within 10 business days of the CIDRE selection. Providers must provide the size of their practice by the number of employees that they employ, and whether the provider is a specialty provider. Health plans must provide their coverage area, QPA geographic area, and must state whether the plan is fully insured or self-insured. Health plans must also state the QPA for the applicable year of the claim dispute.

The QPA, or the median in-network rate, is the primary factor in a final payment determination. The CIDRE must assume the QPA represents a reasonable market-based payment. The CIDRE must begin with the presumption that the QPA is the appropriate OON amount. The CIDRE must also consider the QPA, or the offer closest to it, as the final payment amount.

It is NOT the role of the CIDRE to determine whether the QPA was calculated correctly. Their job is to simply consider the information that is submitted by both parties and consider whether any “additional criteria” is already reflected in the underlying QPA, to assure there will be no “double-dipping.”

The CIDRE can also consider whether information that shows efforts to alter the service codes have occurred, which might result in “up-coding” or “down-coding” billed amounts. Down-coding may show that the QPA is artificially low, for example. However, the CIDRE is permitted to consider “additional criteria” that may lead to a higher payment amount than the QPA.

Such additional criteria includes:

• the level of training, experience and quality of care, as well as the outcome measurements

• the acuity of the patient and complexity of services

• a good faith effort to enter the network by the health plan and provider

• market share held by the provider or facility in the region

• teaching status, case mix, scope of service of facility; or

• contracted rates over the prior four years.

This additional criteria could cause the payment rates to increase for providers, so it’s likely that providers will include as much of this as possible in their submissions. Part 2 rules made it clear that the IDR entities will not give equal weight to both the QPA and additional factors, and that the IDR entities will be instructed to “select the offer closest to the QPA” unless the certified IDR entity determines that credible information submitted by either party is materially different from the appropriate out-of-network rate.

If the “credible information” demonstrates that the QPA is “materially different” than what an appropriate payment for the OON service should be, the CIDRE may choose a higher amount.

The CIDRE cannot take into account:

• a provider’s usual and customary charges

• a provider’s “billed charges”

• rates paid by any public payer payment or reimbursement rates such as Medicare, Medicaid, CHIP or TRICARE, or past arbitration decisions as a precedent. That is not to say that a plan using referenced-based pricing in place of a network, for example, cannot use some form of rating above Medicare rates (such as 150% of Medicare).

The interim final rule clarifies that the CIDRE cannot consider which “offer” is closest to 150% of Medicare; however, the federal departments noted that in-network contracted rates are frequently based on a percentage of Medicare rates. Because the basis of the Qualified Payment Amount is the in-network contracted rates, if the QPA is calculated using a percentage of Medicare, then the CIDRE can take into account this percentage of Medicare value. In this case, the percentage of Medicare value represents the QPA and not a particular offer from the disputing parties.

In a nut-shell, “you can’t come in with a 150% of Medicare offer, but if the QPA is based on a percentage of Medicare, then that can be taken into account by a CIDRE,” stated Chris Condaluci, Self-Insurance Institute of America’s legal counsel, on a recent podcast interview with me on the

Independent Dispute Resolution Process rules (Benefits Executive Roundtable, S3 E8, https://advancedbenefitconsulting.com/s3e8-no-surprises-act-independent-dispute-resolution-process-how-it-will-work/, air date Nov. 2, 2021).

The parties may continue to negotiate after the IDR process begins. If an agreement is reached, the initiating party must inform the federal departments within 3 business days after agreement, and the final payment must be made no later than 30 business days after they have reached agreement. If the parties cannot agree on a payment rate, the CIDRE must make a final payment determination 30 business days after its selection. The federal departments may extend the 30-business day period on a case-by-case basis if the extension is necessary to address delays due to matters beyond the control of the parties or for “good cause.”

The determination of the IDR entity is binding on the parties and is not subject to judicial review, except in narrow circumstances, such as fraud. The IDR process will use a “baseball-style” arbitration process, meaning that the CIDRE is required to pick one of the two “offers” which is closest to the QPA.

The amount of the offers will determine that amount. It could be that the QPA itself is the final amount, or it may be higher or lower than the QPA, depending on the offers submitted.

All in all, as I said, it will be a complicated process, with a long-learning curve.

CAA BROKER COMPENSATION DISCLOSURE

I’ve already provided information on broker compensation disclosure in past articles, as have numerous other authors. In summary, I will just provide the basics of this part of the CAA.

Under existing ERISA rules, group plans may not engage in “prohibited transactions’’ with “parties-in-interest.” A service provider is a “party-in-interest.” But there is an exemption if the services provided are necessary, provided under a contract or arrangement that is reasonable, and provided for reasonable compensation. The CAA amends these rules to place new requirements on plans. Under the rules, no extension or renewal of a contract or arrangement for services between a “covered plan” and a “covered service provider” (CSP) is reasonable unless the terms of the CAA are satisfied. A “covered service provider” (CSP) includes brokerage and consulting services.

A CSP must disclose a summary of services and a description of “direct” and “indirect” compensation reasonably expected to be received (moreover); changes to disclosed information must also be reported.

These rules do not apply to government employer plans exempt from ERISA. The effective date was Dec. 27, 2021; and it does not apply to contracts executed prior to Dec. 27, 2021. According to guidance in the Field Assistance Bulletin that was issued, regulations will not be issued. Brokers CalBrokerMag.com will need to distribute these notices with renewal dates going forward.

Under the CAA, the term “covered plan” means a group health plan. The term “covered service provider” means a service provider that enters into a contract or arrangement with the covered plan and reasonably expects $1,000 (as adjusted) or more in compensation, direct or indirect, to be received in connection with providing brokerage or consulting services. The term “compensation” means anything of monetary value, but does not include non-monetary compensation valued at $250 (as adjusted) or less, in the aggregate, during the term of the contract or arrangement. The term “direct compensation” means compensation received directly from a covered plan. The term “indirect compensation” means compensation received from any source other than the covered plan, the plan sponsor, the covered service provider, or an affiliate. The term “responsible plan fiduciary” means a fiduciary with authority to cause the covered plan to enter into, or extend or renew, the contract or arrangement.

SOMETHING TO PURSUE PLAN COMPLIANCE

I know that I’ve given you a tremendous amount of information in this article. To summarize the To-Dos for plan sponsors, they should be sure to comply with the ERISA and ACA requirements (old), the CAA and TiC rules (new), and understand how the No Surprises Act and CAA will change the marketplace to a certain extent. There are administrative tasks that plan sponsors must complete to be in compliance with the No Surprises Act, which were spelled out in this article (ID cards, provider directories, notices to employees, to name a few). Much of the TiC requirements will be performed by outside vendors, but plan sponsors will need written agreements with them.

All of these changes could and likely will increase plan costs, so employer plan sponsors should be prepared to adjust their budgets if necessary.

As plan sponsors navigate through the old and new rules and compliance requirements, they rely on service partners, such as their brokers or consultants, to help them. These relationships grow stronger with time and assistance. Just remember, as I said in the beginning of this article, we’ll get through it, as long as we work on it and stay positive. So, as you work with those plan sponsors, assisting them with Something Old, Something New,

Something Challenging and Something to Pursue, I hope that you find this article helpful to all of you.

Author’s Note: I’d like to thank Marilyn Monahan of Monahan Law Office for assisting me with my client seminar/webinar preparation and participation, and therefore her assistance with this article. Marilyn can be reached at (310) 989-0993, or at marilyn@monahanlawoffice.com.

DOROTHY COCIU is the president of Advanced Benefit Consulting, Anaheim, Calif. and VP of Communications for the California Agents & Health Insurance Professionals (CAHIP, formerly CAHU). She is the host of the Benefits Executive Roundtable Podcast and is a frequent contributor to CalBroker magazine and other written publications. She is a benefits broker/agent specializing in mid-size and large group health plans, ERISA, ACA, CAA, TiC and other areas of health plan compliance.

She is also a frequent CE class instructor for NAHU, CAHIP, its local chapters, SIIA and other professional associations. She can be reached at 714 693 9754 x 3, or at dmcociu@advancedbenefitconsulting.com.

References & Resources:

ERISA Resources: U.S. Department of Labor, Employee Benefits Security Administration (EBSA):

• Reporting and Disclosure Guide for Employee Benefit Plans

• Compliance Assistance Guide: Health Benefits Coverage under Federal Law, including Self-Compliance Tool for Part 7 of ERISA: Health Care-Related Provisions

• Understanding Your Fiduciary Responsibilities under a Group Health Plan

• An Employer’s Guide to Group Health Continuation Coverage under COBRA

• J. Hanley, Deskless Yet Informed, Benefits Quarterly (4th Quarter 2019)

DOL Voluntary Delinquent 5500 filing – DFVCP Fact Sheet at: https://www.dol.gov/sites/dolgov/files/ebsa/about-ebsa/our-activities/resource-center/faqs/dfvcp.pdf.

CAA Resources: Department of Labor (DOL)

• DOL: Self-Compliance Tool for the Mental Health Parity and Addiction Equity Act (MHPAEA): https://www. dol.gov/sites/dolgov/files/EBSA/laws-and-regulations/laws/mental-health-parity/self-compliance-tool.pdf

• DOL: Understanding Your Fiduciary Responsibilities under a Group Health Plan: https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/publications/understanding-your-fiduciary-responsibilities-under-a-group-health-plan.pdf

Centers for Medicare & Medicaid Services (CMS)

• CMS: Website on Surprise Billing: https://www.cms.gov/nosurprises

• CMS: Model Disclosure Notice Regarding Patient Protections Against Surprise Billing: https://www.cms.gov/filesdocument/model-disclosure-notice-patient-protections-against-surprise-billing-providers-facilities-health.pdf

• CMS: Federal portal where providers and plans will submit their payment disputes: https://www.cms.gov/nosurprises/consumer-protections/Payment-disagreements.