September is Life Insurance Awareness Month

In this Q&A, we share the perspective of several life insurance leaders about the present and future of this important offering.

CalBroker: Given the economy, how do you see inflation impacting life sales? Are you seeing any new life insurance trends or new business segments that are growing or shrinking?

Kim Rudeen, VP Product Development and Management, Aflac:

There are many factors influencing consumer decisions right now. We saw through the early stages of the pandemic that financial concerns can help make people more aware of healthcare costs and cause them to seek out new and dditional benefits to cover their families. Our 2021-2022 Aflac WorkForces Report found that almost half of employees — and 63% of millennials — purchased at least one new benefit as a result of the pandemic, with life insurance topping the list. Among respondents, life insurance was the most commonly purchased supplemental product, selected by over 1 in 5 employees and 1 in 3 millennials. Additionally, of those offered supplemental insurance, 60% are enrolled in supplemental life insurance, demonstrating that it is a highly popular product. That being said, as consumers tighten their belts, it is especially important to help educate them about the value that life insurance provides. That is why, at Aflac, we focus on delivering value to the consumer on day one with living benefits that help protect their overall wellbeing.

“There are many factors influencing consumer decisions right now. We saw through the early stages of the pandemic that financial concerns can help make people more aware of healthcare costs and cause them to seek out new and additional benefits to cover their families.” — Kim Rudeen

Anthony Di Bernardo, CEO, Flexible Insurance Plans (FIP):

I do not see inflation affecting life sales because there will always be clients who need coverage for either their respective family or business. The amount that is affordable is another issue in light of these inflation and recession pressures. I don’t see too much difference in business segments growing or shrinking.

Aguirre, Gryphon Financial

Inflation has given us an opportunity to further market Life designs, specifically over-funded Indexed universal life (IUL) that have the potential to grow a death benefit over the years. This strategy has been useful with clients that fear the erosion of their future death benefit protection by inflation.

CB: Are you seeing more carriers or producers expand their product offerings beyond Life? Like financial advising? Health? Ancillary products? In your view, is this a successful business strategy?

Rudeen, Alfac

At Aflac, we are focused on supporting the overall wellness of our policyholders. For life insurance, that means not just covering the obvious — death of the insured — but also living benefits that can have an effect on their well-being, such as chronic illness, financial health and mental health.

For example, we recently introduced BrightDime as an added-value benefit. BrightDime is a financial wellness platform that gives employees tools and knowledge to build emergency funds, plan for future expenses and prepare for the unexpected. Providing employees access to an Aflac-funded financial wellness program can help them gain confidence in their financial situations and can help address employers’ challenges of lost productivity and retention.

Di Bernardo, FIP

I do see more long-term care being important coverage for late baby boomers because people are living longer, but their health is eroding. I also see more annuities being sought by clients to diversify their portfolios. They can add guarantees to offset risk associated with their investments. Those reps who don’t adapt to these concerns are missing opportunities to help their clients.

Aguirre, Gryphon Financial

Yes. More advisers are now branching out to offer index annuities. This does offer more opportunity for success, because there will always be a percentage of people who cannot qualify for Life insurance—so the adviser can pivot to an index annuity to provide double-digit tax-deferred returns. We have also seen more LTC, disability and Medicare plans being sold by Life advisers.

CB: We see brokers and agents beginning to add life products for clients. They look for training, product access, marketing and leads, and home office support for case design. Are you partnering with them? And if so, what resources do you offer to support them?

“I do not see inflation affecting life sales because there will always be clients who need coverage for either their respective family or business.” —Anthony Di Bernardo

Rudeen, Alfac

We offer robust marketing support for our brokers and agents, including quick reference guides, tip sheets, flyers, product videos, claims forms, etc. We’re continuously publishing new materials to be sure agents and brokers have all they need to sell and promote products.

At Aflac, we want to help our agents and brokers to explain life insurance and other supplemental policies in simple, easy to understand terms so consumers can make the decisions that are best for them.

Di Bernardo, FIP

I help when I can with making introductions to those agencies that offer full support for independent agents searching for that help. My staff members do that for me and for our reps.

Aguirre, Gryphon Financial

We believe that the worst thing an advisor can do is go directly to the home office to identify a Life solution for a client. The home office is going to be a wealth of knowledge for perhaps two to three products that they offer. When our advisors come to us with a Life case, we utilize a combination of software and experience to determine which of the 35+ Life carriers has the solution that will best fit their client

CB: What characteristics and talents are needed to be a successful life sales agent? What skills should new producers develop? If you were mentoring

a life agent, what would be your primary message?

Rudeen, Alfac

Life insurance can be complicated, so it really starts with education. Helping potential customers understand the differences between whole and term life insurance, as well as final expense insurance and how much life insurance they need is all part of helping to market the product well. Another component is educating consumers about the living benefits that life insurance can provide to show the full value of a life insurance policy to the insured and their loved ones.

Di Bernardo, FIP

Lots of patience, persistence and good listening skills. Having immense knowledge in your discipline doesn’t hurt either. Having resources to help — CPA’s, attorneys, actuary’s, chief underwriters — is extremely beneficial.

Knowing who you can lean upon when asked difficult questions or need help developing a complicated case is extremely important. I used to tell our reps when I ran a more diverse agency that the three most important words you can say to a client is “I don’t know — but I know where to get answers for you.” Having those resources in place makes the difference.

Aguirre, Gryphon Financial

Life sales agents need to be patient, intuitive and empathetic, while also being able to help clients that want to protect their assets and loved ones with sound financial planning. Our primary message to a new Life sales agent would be to “lean on us/your Independent marketing organization.” We have decades of sales and product experience that you can’t absorb in a carrier webinar.

“When our advisors come to us with a Life case, we utilize a combination of software and experience to determine which of the 35+ Life carriers has the solution that will best fit their client.” — Ryan Aguirre

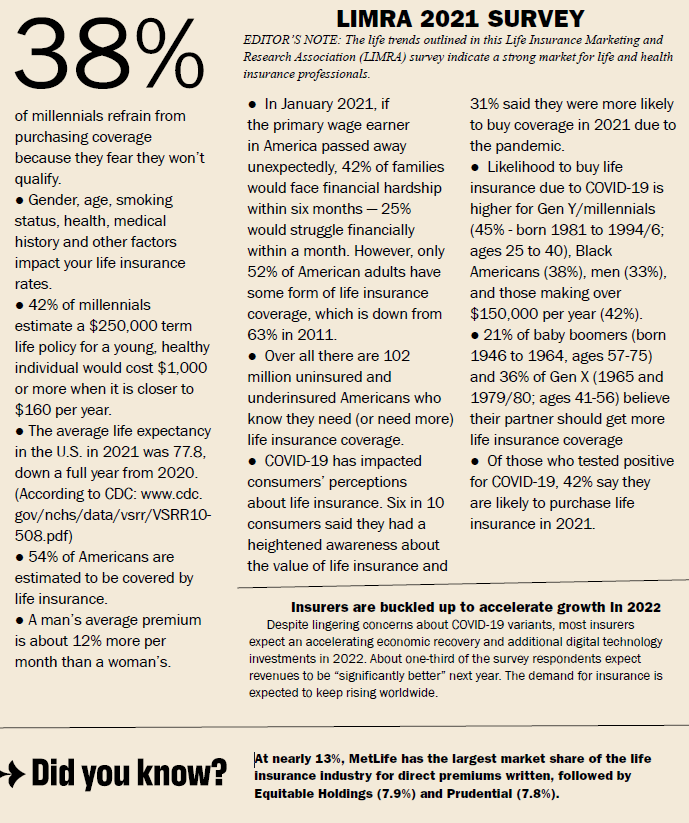

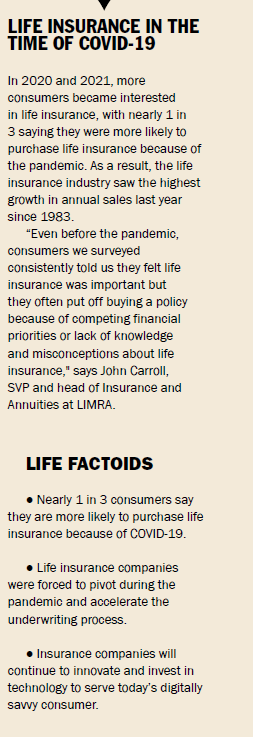

Life Insurance Stats & Facts