BY MARGARET STEDT

THE MEDICARE focused agent should have a clear understanding of the enrollment periods of Medicare A and B and the hierarchy of the periods that apply. This is especially important as more and more individuals are working well past their 65th birthdays.

Another group to consider is the younger disabled individuals who qualify after 24 months on Social Security benefits. Also, many agents have had to address the challenges in assisting a number of Medicare eligible individuals that stayed on their COBRA plans or individual plans and had waived their Medicare coverage to save money or to continue on those plans while not realizing the later issues and enrollment delays, not to mention possible penalties and costs.

Initial Enrollment Period (IEP)

The Initial Enrollment Period applies to the individual turning age 65. If the individual is eligible for Medicare when they turn 65, they may enroll in Medicare Part A and/or Part B. This is a 7-month period that begins three months before the month the individual turns 65, the month of their birthday, and three months following.

Note: if the birthday is the first the month then the seven months move back a month. As an example, for an individual with a Nov. 1 birthday, their IEP begins on July 1 and their effective date would be Oct. 1, if they sign up in one of the three months preceding.

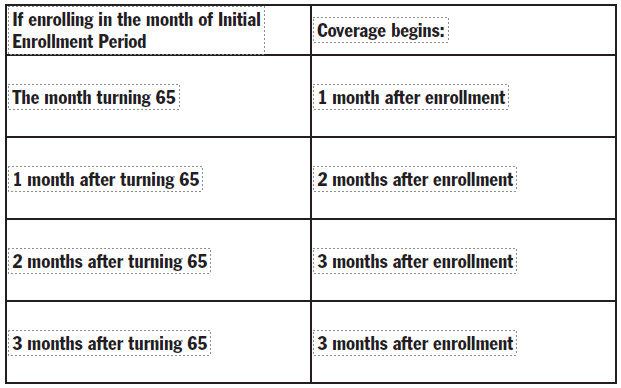

If an induvial waits until the last four months of their Initial Enrollment Period then their coverage will be delayed as follows:

>If enrolling during the month the Initial Enrollment Period Coverage begins, individuals on Social Security Disability for 24 months will be automatically enrolled in Medicare at the 25th month.

Note: they will have an Initial Enrollment Period when they turn 65. It is also important to note that if they decline to be covered when first eligible and continue on their COBRA or Individual Plan, they will need to wait for the General Enrollment Period to apply for Medicare coverage and may be subject to penalties.

Special Enrollment Period

Once the Initial Enrollment Period ends, the individual may sign up for Part A and Part B but only if they meet certain requirements of the Special Enrollment Period (SEP). If an individual is covered under a group insurance plan based on current (active) employment they have an SEP to sign up for Part A and/or Part B at time as long as the individual or the spouse is working and covered by a group health plan through an employer or if in a union plan based on work for coverage.

The effective date for coverage varies, as it is based on when the enrollment request is made, if enrolling during the SEP. After Social Security receives and processes the request for enrollment, the Medicare coverage typically begins the first month or at the individual’s option, the first day of any of the following three months. Usually, a late enrollment Part B penalty does not apply. The SEP also does not apply to individuals with End-Stage Renal disease (ESRD) and coverage under Veterans Affairs or Individual Health Insurance Market Place Coverage.

Important Note: COBRA, Individual, and Retiree plans are not considered as creditable coverage based on current employment. People under these plans are not considered eligible for an SEP and must apply during the General Enrollment Period.

“When I meet with prospects I remind them that timing is everything in Medicare.”

When I meet with prospects I remind them that timing is everything in Medicare. Their delays to enroll into Medicare could result in penalties for Part A and for Part B and in a delay in coverage. Individuals who lose their group coverage have up to 8 months to sign up for their Part B. The individual must have both Medicare Part A and Part B to sign up for the Medicare Advantage or Medicare Supplement Plans. They may have either Part A or Part B to enroll in the Stand-Alone Prescription Drug Plan. They only have 63 days after the loss of their employer coverage to enroll in a Medicare Advantage Plan or Stand-alone Part D Plan. Individuals have 6 months from the initial date of their Part B to sign up for a Medicare Supplement Plan on a guaranteed issue basis.

General Enrollment Period

If an individual does not sign up for Part A and/or Part B when they were first eligible and they did not qualify for a Special Enrollment Period, then they must wait until the Medicare General Enrollment Period (GEP). This period runs from, January 1 to March 31 for enrollment and coverage begins the following July 1.

In most cases the individual, if signing up for Part B of Medicare, will be subject to the Part B late enrollment penalty of 10% for each 12-month period they were not covered under Part B. The penalty continues as long as they have Part B. Don’t neglect reviewing the possible Part D penalty as well for the delay in coverage under Part D (Medicare Advantage Prescription Drug Plan or a Stand-Alone Prescription Drug Plan.) Note that Veteran Drug coverage is considered creditable coverage for Part D.

Refer to www.medicare.gov for information regarding the Part A late enrollment penalties.

Enrollment period hierarchy

In the case when an individual qualifies under more than one enrollment period the order that applies is:

1. Initial Enrollment Period

2. Special Enrollment Period

3. General Enrollment Period

The Special Enrollment Period and the General Enrollment Period are only available after the end of the Initial Enrollment Period. Section 1837(i)(1) of the Social Security Act outlines the eligibility for SEP enrollment.

Want to know more — and to help your prospects who have these specific types of questions?

- When and can I enroll when living outside the U.S.?

- Can I have both Medicare and Retiree Coverage?

- Can I have Veteran’s Benefit coverage and Part A and B of Medicare?

- What happens to my Health Savings Account when I sign up for Medicare?

- I have individual insurance and want to continue on the plan after I turn age 65. What are my options?

You will find the answers in the “Medicare and You” Booklet, the CMS “Enrolling in Medicare Part A and B” booklet and on-line at www.medicare.gov and www. socialsecurity.gov websites.

For those of you who are members of the National Association of Health Underwriters (NAHU), review Don Mangus’ article in the July 2021 issue of the Association’s Benefits Specialist Magazine. NAHU also has great new flyers available that detail some of the basics about Medicare including enrollment. Find them online in the Medicare Section under the Members Only part of www.nahu.org.

Many individuals and Human Resource managers do not understand the Medicare Enrollment Periods and eligibility. Your prospects and clients could be subject to delays in coverage, penalties and added medical and prescription drug costs just because of the uninformed decisions they make when delaying their Medicare Part A and B coverages. Especially if their health coverage is not creditable for later enrollment. You as an informed and knowledgeable agent are a great resource and a trusted advisor who can help them to understand their options and the possible risks.

MAGGIE STEDT is an independent agent that has specialized in the Medicare market for the past 21 years. She is the immediate past president of California Association Health Underwriters (CAHU) and past president of her local Orange County Health Underwriters Association (OCAHU) chapter. Reach her at”maggiestedt@gmail.com.