3 Tips for Talking to Clients About Risk

Insurance is all about managing risk — not avoiding it

By Bob Ruff

American aviator Charles Lindbergh once said, “Life without risks is not worth living.” Taking educated risks, such as assuming new responsibilities at work or moving to a new city, can be necessary to forge ahead in both our personal and professional lives. Being a risk-taker doesn’t mean being reckless, however — in fact, a survey conducted by my organization, Aflac, found that people who self-identify as risk-takers are more likely to actively take steps to mitigate risks, such as having health insurance or having more than one income stream. These findings indicate that even those of us most inclined to take risks are reliant on checks, balances and safety nets.

Insurance is all about managing risk — not avoiding it — and that’s why it is so important for brokers and benefits consultants to be able to talk to their clients about risk management strategies for their workforce, so they can help their employees take risks that make life worth living.

So, what are the best practices for ensuring these checks and balances are in place, allowing employees’ risks to result in reward?

Zoom out to assess multidimensional risk

After a major pandemic, economic challenges, social injustice anxieties and political unrest, it’s important to zoom out on the risk landscape to help clients identify where their workforces are most vulnerable. For instance, one factor to consider that is more prominent today than it was even two years ago is managing risk to mental health. In fact, our survey found

- nearly 90% of Americans list proactively managing risks to mental health as a priority, compared to 80% who are concerned about the state of the U.S. economy

- 61% who are concerned about the effects of politics on their households

- 54% who are concerned about the impact of COVID-19

Helping clients to see that risk is multidimensional is the first step to uncovering where there are vulnerabilities that could use an additional product offering, added-value tool or other risk management tool.

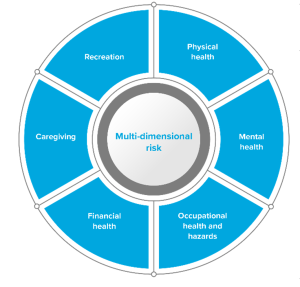

One way to visualize this concept is through a “wheel of risk.” Showing risk as an interconnected wheel can help clients take inventory of the potential physical, mental, occupational, financial, family/caregiving and recreational activities. Every client will have unique employee populations, which can help focus on their distinctive needs. Brokers can then tailor various aspects of their benefits portfolio recommendations to help identify where the employer may need to bolster their benefits offerings.

Understand that risk tolerance is not one-size-fits-all

One person’s acceptable risk is another person’s “not a chance.” That is equally true of going skydiving as it is investing in volatile assets. That’s why it’s important for employers to offer a range of benefits, such as health, disability and life insurance, that employees can opt into based on their age, family situation, medical history and lifestyle. By working with clients to understand the demographics of their employees, brokers can help develop a suite of benefits that workers can customize to fit their needs.

Learn from the risk-takers

Risks are an inherent part of life, but whether those risks include a safety net is up to us. Just as there are some risks that do not discriminate based on age, race or income, there are some benefits that everyone, no matter their risk tolerance, should have available to them. Those include tools and resources to proactively protect mental health and insurance to help safeguard income in the event of an accident or illness.

It’s critical to help clients understand how they can address the many risks their employees face that could have an effect on their health, well-being and, ultimately, ability and desire to engage at work. Although every employee will not be an absolute risk-taker, talking to them about the risks they face in life can help clients build a better benefits strategy, so they can help protect their workforce no matter what life brings their way.

Bob Ruff is SVP, Group Voluntary Benefits at Aflac. With more than fifteen years of leadership experience in the employee benefits industry and deep expertise in market analysis and sales, Bob is passionate about advancing innovation to further the reach and impact of insurance products. He is responsible for overseeing all strategic, operational, and financial aspects of the company’s largest and most profitable division. An approachable and empathetic leader, Bob empowers his team to drive organizational growth by anticipating customer demand and identifying emerging trends.

Contact:

email: RRuff@aflac.com

Website: https://www.aflac.com