Helping the New Medicare Beneficiary Decide

BY MARGARET STEDT

Agents play a key role in helping the new Medicare Beneficiary in deciding what type of coverage and then the plan that best fits their needs. Many of the Medicare Beneficiaries are confused and frustrated as Medicare Coverage is brand new to them with different names, coverages and plan types than what they experienced on either group insurance plans or individual plans (On or Off Exchange).

When meeting with the Medicare beneficiary you should start by asking what their questions and concerns are. Ask what type of coverage they are on now and how it is working for them.

Who are their doctors and do they have relationships with specialists in several Medical Groups? Are they comfortable with the idea of a referral process? Do they travel both inside and out of the country? Is prescription drug coverage important to them and have there been any challenges? These questions will help you inexplaining the options and to determine which plans to consider.

Many times, the beneficiary insists that they want a PPO plan like their current coverage. This needs to be addressed carefully as you explain the difference between a Medicare Supplement Plan and the various types of Medicare Advantage Plans. Never say a Medicare Supplement Plan is a type of PPO plan. In the senior products arena, a PPO is a type of Medicare Advantage Plan.

Agents need to be able to explain the difference between the MedicareSupplement Plans (Med Supps) and the Medicare Advantage (MAPD) Plans.

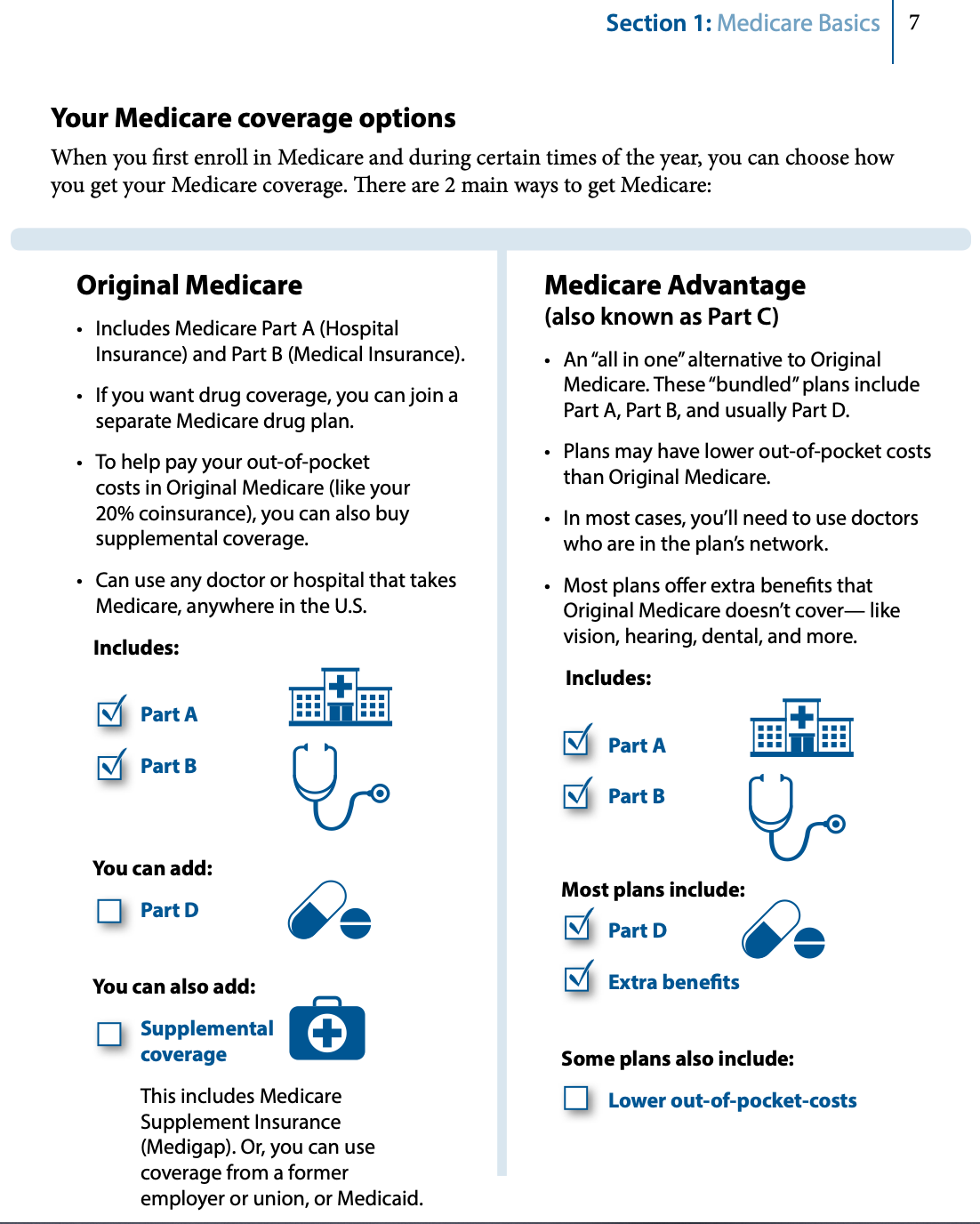

I begin by using Section 1 of the CMS booklet “2021 Choosing a MediGap Plan “(CMS Product No. 02110) that is typically provided with the Medicare Supplement Sales Kit. I find the chart on page 7 helpful for the beneficiary to take notes on.

The first step is to explain about Part A and B of Medicare by reviewing the different parts of Medicare. Note that there is no maximum out-of-pocket for the copayments, deductible and coinsurance amounts of Medicare.

Agents should review the monthly cost for Part B and IRMAA and note that it typically changes each year. The IRMAA (Income Monthly Adjusted Income Amount) for Part B and D may be found on the www.medicare.gov website.

Many times, the beneficiary insists that they want a PPO plan like their current coverage. This needs to be addressed carefully as you explain the difference between a Medicare Supplement Plan and the various types of Medicare Advantage Plans. Never say a Medicare Supplement Plan is a type of PPO plan. In the senior products arena, a PPO is a type of Medicare Advantage Plan.

Agents need to be able to explain the difference between the Medicare Supplement Plans (Med Supps) and the Medicare Advantage (MAPD) Plans.

The next step is to review the two main ways to get Medicare coverage

- by remaining on Original Medicare and enrolling in a Medicare Supplement (MediGap) Plan

- enrolling in a Medicare Advantage Plan (also known as a Part C of Medicare.

I use the chart provided on page 7 of the CMS MediGap Booklet to review the differences in the plans. Once the client understands Medicare Part A and B then it is time to review the difference between Med Supps and MAPD plans.

REVIEWING THE MEDICARE SUPPLEMENT PLANS

These plans are designed to cover the out-of-pocket costs such as coinsurance and copays of Medicare Parts A and B. The Original Medicare Part A and B is the primary coverage (pays first) and the Med Supp is secondary. The plans will only pay if it is a Medicare approved service and Medicare pays first.

There is a monthly premium for the plans. The rates for the most of the plans in California are based on the covered person’s age andresidence zip code or county. The rates will change from year to year based on age and a rating action by the company. If they move to another state, they may keep their plan but will pay the rates for the highest premium rate area.

Medicare Supplement Plans are subject to underwriting and pre-existing clauses apply unless the beneficiary meets a Guaranteed Issue (GI) situation. Agents should review the underwriting guidelines for each company they are representing. While the GI situations follow the CMS and state requirements, there are variations between the companies in the plans that can be offered and some the situations such as voluntary or involuntary termination from a group insurance. Also, if and what plans can be offered to the age 65 Medicare Beneficiary.

In California we have the advantage of the California Birthday Rule that allows the covered person to change to an equal or lower plan (e.g., G to another company’s G or Innovative G or G to an N). The Guaranteed Issue period is on and 60 days following their birthday.

The main benefit to a Medicare Advantage plan is these plans include both Parts A and B and cover most, if not all the deductibles and out of pocket costs associated with Original Medicare. Many Medicare Advantage plans also include Part D coverage (prescription drugs), at no additional premium. Members will still be responsible to pay Part B premiums.

As the plans are designed to cover the copayments and coinsurance amounts of Medicare, they do NOT cover additional services suchas dental, Part D prescription drugs, hearing (hearing aids, exams and screenings), transportation, routine eye care and most glasses andcontacts and most health care outside the United States. However, in California some companies are now offering the Innovative Plans (one company calls theirs Extra) that offer vision and hearing benefits.

The advantages of a Medicare Supplement are:

- Choice of any doctor who accepts Medicare anywhere in the U.S.

This means if the beneficiary wants to see a Johns Hopkins doctor on the East Coast or a doctor at UCLA, they have that option. Of course, they are responsible for all transportation, but at least they have the option. - Med Supp’s are portable, meaning if the covered person moves, the policy moves with them without any underwriting.

- The policy is guaranteed. This means the company cannot cancel the policy for anything other than non-payment. So regardless of the use, the covered person can rest assured that they will always have coverage.

- A MediGap Plan may reduce out-of-pocket costs. Medical costs are fixed and do not vary month to month.

The main disadvantages to Medicare Supplement plans are the premium costs that typically increase each year and no additional benefits. Some companies may offer ancillary benefits such as gym membership, over the counter items, chiropractic and acupuncture and limited overseas travel (depending on the plan). Remember the plans are designed to cover the copays and coinsurances of Medicare. (Plan C & F cover the Part B deductible.) The Medicare beneficiary must enroll in astand-alone prescription drug plan for coverage for their Part D prescriptions drugs.

In addition, there is an issue regarding skilled nursing coverage. If the Med Supp covered person was not admitted to the hospital as they were on observation status and did not meet the three-day hospital stay requirement prior to being admitted into skilled nursing, Medicare will not pay, so the Med Supp will not as well.

If a covered person disagrees with a decision by Medicare for a denial of coverage, there is an appeals and grievance process to request that Medicare revisits the decision.

REVIEWING THE MEDICARE ADVANTAGE PRESCRIPTION DRUG (ALSO MEDICARE ADVANTAGE ONLY)

Part C of Medicare are Medicare Advantage plans. Medicare Advantage plans are approved by Medicare and administered by private insurance companies, taking the place of Medicare. This does not mean the member loses Medicare, as they can revert back to Original Medicare under Medicare guidelines, it just means the health plan will pay out Part A and Part B benefits instead of Medicare.

The main benefit to a Medicare Advantage plan is these plans include both Parts A and B and cover most, if not all the deductibles and out of pocket costs associated with Original Medicare. Many Medicare Advantage plans also include Part D coverage (prescription drugs), at no additional premium. Members will still be responsible to pay Part Bpremiums.

There are several types of Medicare Advantage plans such as Health Maintenance Organization (HMO) Plans, Preferred Provider (PPO) and Special Needs Plans. The plan offerings vary by company and by county. Note the benefits can be no less than those offered by Original Medicare. Depending on the company’s plan there may be a monthly premium. There are plans in some areas also offering a giveback of some or all of the Part B premium.

Medicare Advantage plans may also include additional benefits not offered by Original Medicare, such as, dental, vision and transportation to doctor visits! And many are covering the stay in a skilled nursing facility although the individual was on observation status and did not meet the 3-day prior hospitalization Medicare requirement.

The main disadvantage to Medicare Advantage plans is members typically must use an established network for medical care unless it is an emergency or urgent care. Networks may limit which doctors a member may visit. For most services a referral is required from the Primary Care physician to a specialist or for treatment. (Types of services waiving the referral requirement vary by plan.)

Lastly, a beneficiary must be in an enrollment period to be eligible to join a Medicare Advantage plan in addition to the other eligibility requirements.

You as the agent need to understand the differences and plans and present them clearly for the beneficiary’s understanding.

With any HMO plan, members can change to a primary care physician by contacting the plan and requesting the change. Usually if made before the 15th of the month, they can begin seeing their new primary doctor the first of the next month.

Disenrollment is also simple. If the member changes their mind prior to the plan’s effective date they can cancel the application andenroll in a new plan. If they disenroll after the plan’s effective date, one needs to submit a request in writing. The agent should discuss theoptions and consequences of the disenrollment as there are rules as to new plan eligibility and Part D.

If a member disagrees with a decision of their health plan, say on a drug exception or a denial of coverage for a C-pap machine for instance there is an appeals and grievance process to make the health plan revisit the decision.

Once you have determined which type of coverage the Medicare Beneficiary would like to consider you then can go into the plan details, the prescription drug coverages and other benefits. Remember to always secure a Scope of Appointment prior to discussing the Medicare Advantage or Stand-Alone Part D plans.

Medicare Supplements and the Medicare Advantage Plans offer great coverage options to the Medicare beneficiary. One is not better than the other. It is a matter of which type and which plan best fits their needs both medically and financially. You as the agent need to understand the differences and plans and present them clearly for the beneficiary’s understanding. And, it is important to note that you will be reviewing the plans with your client yearly to continue to determine the plans that best fit their needs!

MAGGIE STEDT is an independent agent that has specialized in the Medicare market for the past 21 years. She is currently president of California Association Health Underwriters (CAHU) and is a past president of her local Orange County Health Underwriters Association (OCAHU) chapter.

MAGGIE STEDT is an independent agent that has specialized in the Medicare market for the past 21 years. She is currently president of California Association Health Underwriters (CAHU) and is a past president of her local Orange County Health Underwriters Association (OCAHU) chapter.

Reach her at maggiestedt@gmail.com.