COVID-19 is on its way out, even though experts say the pandemic isn’t really over until the vast majority of Americans are immune from the virus.

Still, the end is near and contours of life after COVID-19 are taking shape. That goes double so for the U.S. life insurance market, where the pandemic has made its mark over the past 18 months.

“COVID-19 has raised awareness about the important role life insurance plays in families’ financial security,” said David Levenson, president and CEO, LL Global, LIMRA and LOMA. “Our research shows 42% of Americans would face financial hardship within six months if the primary wage-earner were to die unexpectedly.”

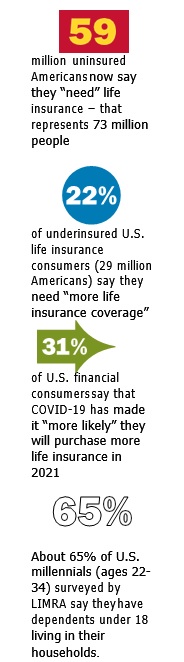

The life insurance sector seems to be in a prime position to help Americans who are either underinsured or have no insurance at all. A recent study from LIMRA tells the tale:

“… it’s understandable as the current data finds 43% of millennials are more concerned than other generations about leaving their dependents in a difficult financial situation if they should die or burdening others with burial/funeral expenses,” the report stated.

Key life insurance market issues in a post-COVID-19 world

The data does point to significant change in the U.S. life insurance market with these factors setting the tone for a new landscape for consumers and insurance professionals alike:

Young Americans at risk. The LIMRA study showed that over 50% of millennials have no life insurance coverage. “The good news is 48% of millennials say they plan to buy coverage in the next year,” Levenson said. “While we know not all will follow through, our industry needs to help these young adults get the appropriate coverage that will protect their families.”

Huge gap in life insurance needs.

LIMRA also points to an estimated life insurance coverage gap of $12 trillion across the U.S. life insurance market place, with an average per-person shortage of about $200,000 in needed insurance.

Low enthusiasm among lapsed customers. A separate report from Deloitte showed that 14% of lapsed life insurance buyers and 20% of customers who’ve never had mortality life insurance coverage are even considering new life insurance policies.

Declining COVID-19 cases are a factor for non-buyers. One other point from the Deloitte study — 35% of Americans who thought about buying life insurance during the pandemic decided against it, primarily because COVID-19 cases were dropping in their communities.

Declining COVID-19 cases are a factor for non-buyers. One other point from the Deloitte study — 35% of Americans who thought about buying life insurance during the pandemic decided against it, primarily because COVID-19 cases were dropping in their communities.

A forward looking snapshot: what experts say the post-COVID-19 life insurance landscape will reveal

How is the post-COVID-19 life insurance landscape evolving in the second half of 2021? There are myriad factors in play, all of which should keep life insurance brokers and agents busy as the pandemic wanes and as new changes take hold in the industry.

After canvassing multiple life insurance professionals, these trends seem to be at the top of the list for the rest of the year:

E-Sign here to stay. Industry experts say that life insurance companies, like the rest of the world, have had to adapt and change the way they do business during the recent COVID-19 pandemic.

“Some of the recent changes have been positive,” noted Jeff Busch, an insurance specialist at Lift Financial, in South Jordan, Ut. “For example, many life insurance companies have more widely accepted digital signatures using technology such as DocuSign and e-applications on their own platforms.”

Speeding application approvals via digital technologies. Another technology-based aspect shift in the life insurance market is the acceptance of what is called accelerated underwriting.

“During the pandemic, para-med exams were not feasible, which led to many companies expanding their digital underwriting guidelines using things like medical background checks in lieu of an in-person para-med exam,” Busch said. “Now, a person in good health applying for life insurance could be approved in a matter of days compared to the traditional process that, in some cases, could take several weeks. We’re seeing insurance companies offering death benefits up to $1 million using accelerated underwriting.”

Younger Americans seeing the light?

Life insurance professionals are starting to see millennials get off the fence and into a life policy, largely driven by COVID-19 realities.

“The number of life insurance policies sold increased by 11% in the first quarter compared with the same period last year,” said Linda Chavez, founder & CEO at Seniors Life Insurance Finder in Los Angeles. “That’s the largest increase since 1983, as COVID-19-related deaths drove many consumers to buy coverage. We saw sales rise more than 20% in the first quarter. From our vantage point, younger consumers appear to be buying insurance in greater numbers than other age groups.”

No firm stance on COVID-19 underwriting. Life insurance companies seem to be seeking their own counsel on extending (or not extending) COVID-19 underwriting restrictions.

“Insurance policies have not really evolved since the pandemic, but the underwriting guidelines did change dramatically, especially for higher risk individuals,” said Gordon Conwell, president at Gordon E. Conwell Associates, Inc., a family-owned life insurance agency in Flourtown, Pa.

“Some companies have recently removed their COVID-19 underwriting restrictions, whereas others have not. I’ve talked to some carrier underwriting departments who’ve told me recently they have no current plans to remove their restrictions.”

Conwell said it “makes no sense” why some carriers have removed COVID-19 restrictions but others have held firm. “That’s an important fact for higher risk consumers so they can avoid being quickly declined for life insurance,” he said.

“Anyone who was declined for life insurance last year and was told they were declined due to COVID-19 or the resulting insurance underwriting restrictions should re-apply now.”

A new push on “temporary” life insurance. As a life insurance agent, Busch said he’s happy to see people of all ages applying for the coverage their family needs. Accelerated applications, however, have triggered major delays in processing applications, and that’s a problem right now.

“A combination of record application numbers and processors being unable to work or go to the office has caused some frustration on all sides of the plan,” Busch said. “On the upside, we’re seeing a new policy feature roll out: temporary insurance coverage.”

Busch said temporary life insurance allows an applicant to be covered by the policy at the time of application as long as the first premium payment is paid to the agent when signing a life insurance policy application.

“This covers the insured from that time as long as the policyholder is deemed insurable,” he stated. “Should a policyholder pass away during the underwriting process, the insurance company will finish underwriting and still pay the claim to the beneficiaries, if they determine the holder was insurable prior to passing away. So, applicants should pay that initial premium at the time of application.”

The takeaway on life insurance in a post-COVID-19 market

In the first half of 2021, many U.S. insurance companies saw record numbers of applications for life insurance. “That’s good news,” Busch noted. “It seems people are evaluating their financial lives and acting on the realization that their family needs some protection from uncertainty.”

That said, industry professionals who engage directly with life insurance clients should expect to do their fair share of hand holding as life returns to normal.

“For example, clients may be asking if their life insurance policy will still pay out to beneficiaries if the client passes away due to COVID-19 complications,” Busch said. “The answer is yes, as long as the client’s premiums are paid up-to- date and the policy is in good standing.”

Consequently, insurance specialists should advise their clients to check on their own policy to make sure the life insurance policy offers the needed overage.

“The worst thing that can happen to a life insurance consumer is to think you have coverage when you really don’t,” he added.

Author’s Note

Thank you to the following people who served as sources:

Jeff Busch via Nick Vecore M&O Marketing nick.vecore@mandomarketing.com

Linda Chavez

Seniors Life Insurance Finder chavezlindaslif@gmail.com

+1 (213) 568-1822

Gordon Conwell, III

800-380-3533 (also text-able #) Americanterm.com

BRIAN O’CONNELL

is a senior analyst at InsuranceQuotes.com and a freelance writer based in Bucks County, Pa. A former Wall Street trader, he is the author of the books, “CNBC

Creating Wealth” and “The Career Survival Guide.” His work appears regularly on major media platforms like Fox Business, U.S. News, The Motley Fool, TheStreet.com and many others.