What a legal structure can and can’t do for you

BY PHIL CALHOUN WITH DANNIEL WEXLER

In this article, we will cover information to consider when making key planning decisions. Health insurance professionals will learn how legal structures may protect their personal and business assets and provide allowable tax advantages that can help accomplish many planning goals.

“The important planning issues we consistently see for health insurance professionals and other advisors includes knowledge of legal structures, estate planning, tax and financial considerations as well as revenue protection in all life events,” explains Danny Wexler, counsel to Strazzeri and Mancini LLP.

The purpose of planning is to develop a personalized map you can follow for 5, 10 or more years. It is meant to help you arrive at your desired ending point or address unexpected events along the way. The assumption that a legal structure will address all the unique and significant issues insurance professionals face will be clarified.

Keep in mind there are variables for each person that may increase or decrease the need and type of planning tools utilized. “If you work solo and plan to continue solo, your needs are different from working with a partner,” Danny clarifies. “If you are employed by either an insurance carrier or insurance agency, your needs are unique.”

Asset Protection

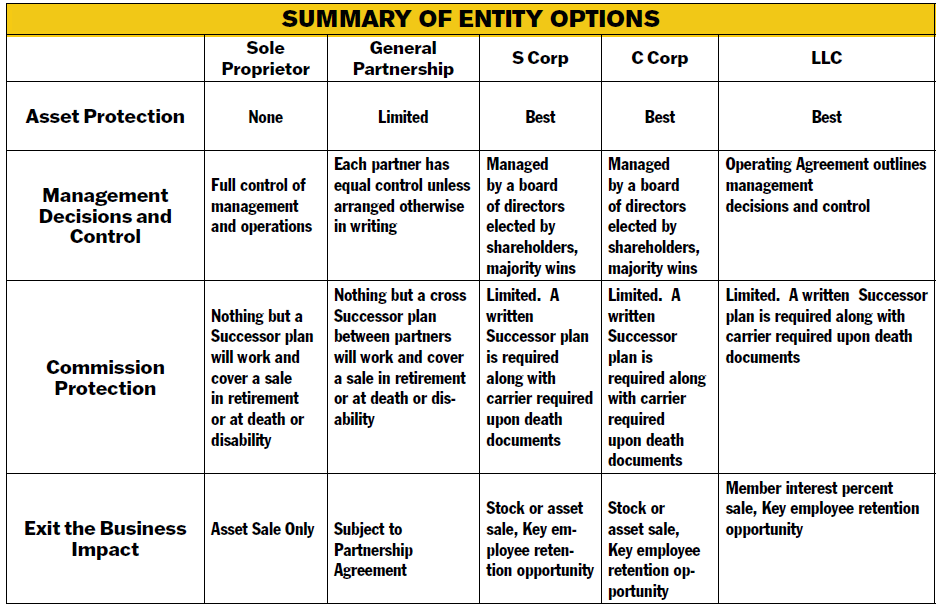

Asset protection is best provided in a legal structure. The table below outlines various legal structures. While each structure comes with costs and management requirements, the decision of which entity is best is based on your needs. If you work solo, have a few “partners” or work as part of a larger organization your decision of the legal structure needed will be based on your plan. In most cases insurance professionals are either solo now and want to stay solo or some may consider working with one or more solo brokers and form a new legal entity. Since asset protection is key to this discussion, we need to address how assets can be protected.

“Creditors, such as banks or even insurance carriers, can file a lien or lawsuit on anyone, an individual or corporation,” says Danny. “All legal action causes difficulties when individuals and/or entities are sued. Finding solutions to lessen the impact of a potential or actual lawsuit is the planning priority. Your legal entity can protect your personal assets when formed and operated correctly.”

One example is when a lien or lawsuit is filed on a corporate entity. “Personal assets are held outside of an entity and therefore are often protected,” he notes. “Personally held real estate, bank accounts, qualified retirement accounts, life insurance cash value, and other assets held outside the entity may be protected from creditors of the entity.”

Tax Advantages

Tax considerations outlined in the chart show the benefits of a corporate structure. “The potential expense of $800 annual minimum tax an entity is required to pay can be worth the expense, considering the benefits of enhanced tax planning,” Danny advises. “The advantage of expensing allowable business items on a pretax basis can provide a significant tax advantage. Consult with a personal tax planner on allowable expenses.”

Protection of residual commissions

Our final concern is commission protection and how a legal structure works in the case of a life event, death, disability or divorce. This is a concern for nearly all active solo brokers and many insurance professionals in a small agency.

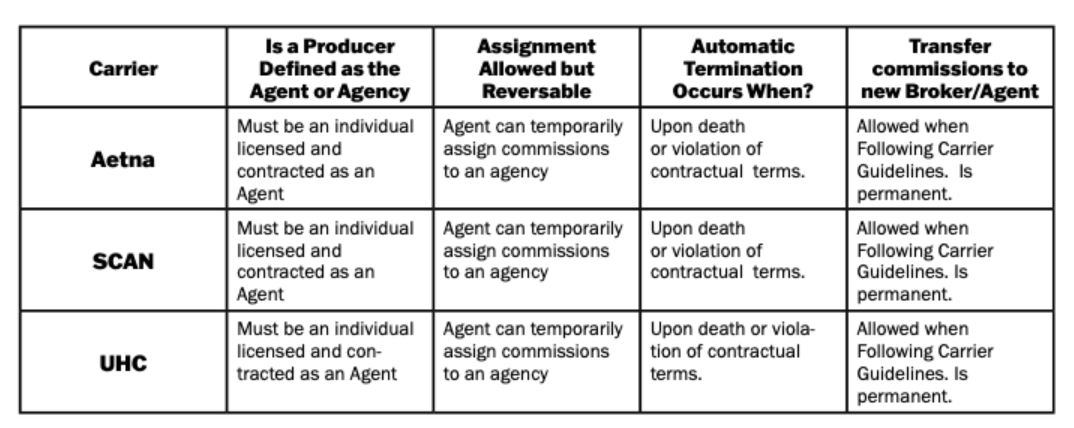

If the goal is protecting commissions in all life events, then the question is — will a legal entity provide this protection. “Legal entities are wonderful for asset protection and tax planning but have narrow protection for the earned commission of individuals or members and shareholders of an entity,” Danny says. “This is because carriers contract with insurance professionals. Health commissions earned from an insurance carrier are paid to a licensed health insurance professional. Commissions directed through assignment to an entity are at risk.”

The table above outlines how a corporation does not have an insurance license, does not contract with health insurance carriers, does not sign an enrollment application for a client applying for a health plan, and does not get certified annually for MAPD and PDP plan enrollment. “Based on a review of the producer agreements from top carriers it appears clear that only an individual who is licensed, required to meet continuing education requirements, certified with AHIP and all carriers paying the producer annually, signs the enrollment application for a client, and remains in good standing and alive will continue to receive the commissions they earned when submitting applications to the carriers with whom they have a personally executed producer agreement,” states Danny. “Given these conclusions, the legal structure a broker selects will have no impact on their commission payments now or in the future.”

Summary

A properly developed and managed entity can be an excellent defense of personal assets in a lawsuit and may offer tax savings opportunities for the owner or shareholders. Legal entities will not protect commissions when the health insurance professional experiences a life event as stated in the four carrier producer agreements referenced in the table above. Carriers will transfer commissions when a broker passes away and they have documents showing how commissions will be handled upon death.

One option is a signed commission protection plan with an identified successor that outlines what to do in the event of the health insurance professional’s death or disability. This document — along with each carrier’s required documents, such as a death certificate and estate executor endorsement — will likely ensure a successful result.

Active brokers are encouraged to learn more about how to protect their commissions while they remain active in the business. Active health insurance professionals interested in solutions to get 100% commission protection can email the author or arrange a 15-minute call.

For legal and tax advice on this topic please consult your local professional.

PHIL CALHOUN worked for an M&A firm after completing his MBA, became licensed in 1990 and has set up several LLCs. He’s worked for hospitals, had business partners and has joined and separated with and from LLC business partners. He sold and purchased commissions from agencies and individuals. He has evaluated hundreds of businesses in numerous industries, many which were successfully sold. His firm has recently acquired health books from 12 retiring health brokers and he and his colleagues are successors for several active brokers. Phil consults with active and retiring health insurance professionals. He continues to operate agencies with group, Medicare, and IFP business with his team.

Contact: phil@commission.solutions, 800-500-9799

DANNY WEXLER a New York native, completed law school at USC. He is recognized as one of Forbes Top 100 estate planning attorneys in the U.S. Danny also manages the Orange County Exit Planning Institute, a professional collaborative of CPAs, bankers, attorneys, financial planners and business brokers. He is of counsel to Strazzeri and Mancini LLP. Danny coauthored “Exit Planning for Medical Doctors” and has written many legal reports and articles. He co-owned a law firm and now collaborates with insurance professionals to assist them with their client’s exit and estate planning needs.

Contact: danny@strazzerimancini.com, 858-200-1900