How to Turn a Problem into an Opportunity

BY ED MCCLEMENTS, JR.

You can increase your book of business by helping clients and prospects deal with the challenges presented by California’s retirement plan mandate — even if you are not a retirement planner

RECENTLY POSTED DATA on the California State Treasurer’s website reveals there are more than 200,000 California businesses that have not yet complied with the CalSavers mandate (if you are unaware of CalSavers, please see the sidebar where the essential details of this law are outlined, before reading further.)

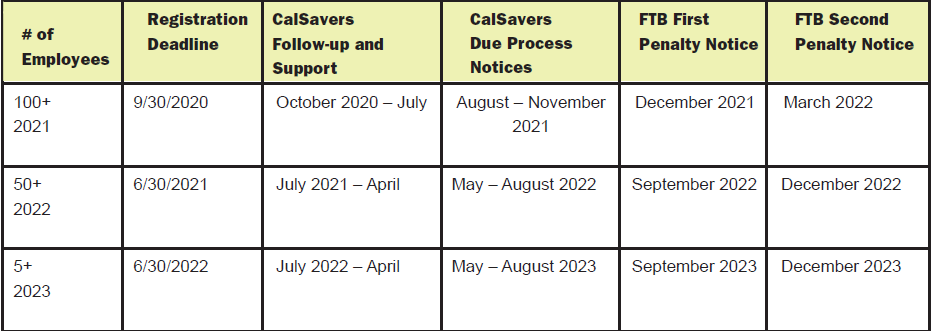

In a nutshell, California law now requires every employer with five or more employees to either offer workers a qualified retirement program (such as a 401k) or enroll in the state-sponsored CalSavers program. CalSavers is a highly ambitious law designed to address the over 7 million working Californians who do not have access to a retirement plan at work. The CalSavers law (SB 1234, signed by Gov. Jerry Brown on 9/29/2016) was the legislature’s response to this societal and economic issue. CalSavers is now well into its implementation phase and deadlines for enrollment have already passed for two out of three tiers of employers, and for the final tier (employers with 5-49 employees) the deadline is June 30, 2022.

CalSavers is a highly ambitious law designed to address the over 7 million working Californians who do not have access to a retirement plan at work.

Even if retirement planning is not a part of your practice, as a top-notch employee benefit broker, your clients probably consider you a trusted advisor. Consequently, you might soon be asked your opinion on CalSavers. That’s because the State of California has, up to this point in simply encouraged employers to voluntarily comply — there have been no enforcement penalties for non-compliance yet issued. But that is about to change. CalSavers has earmarked a multi-million dollar inter-agency expenditure to fund the Franchise Tax Board’s (FTB) efforts to penalize employers that have not yet signed up for CalSavers or certified their alternative retirement program with the CalSavers website. Once FTB letters are issued, if the targeted employer remains noncompliant for 90 days, they will face a $250 penalty per eligible employee. If noncompliance extends beyond 180 days, the FTB will seek to collect an additional $500 penalty per eligible employee.

The CalSavers Retirement Savings Board official meeting minutes indicate that over 2,000 large employers (those with 100+ employees) will be receiving the first wave of those penalty notices very soon. Although the exact mailing date is not known, it is expected to be in January 2022.

Other information in these Board minutes (which are publicly available at https://www.treasurer. ca.gov/calsavers/meeting/index.asp) indicate that CalSavers has already culled State Wage tax reports and cross referenced them with Federal IRS and DOL records to identify the 300,734 California employers that do not already have a qualified retirement plan in place. Since the start of CalSavers, 66,394 employers have either signed up with CalSavers or registered an alternative program — that leaves 234,340 employers who will need to fall into compliance very soon or face thousands of dollars in penalties.

This potential problem can be turned into a significant opportunity for those brokers who take the time to understand both CalSavers and the various alternatives employers can implement to be compliant. Inevitably, the 234,340 employers mentioned above will find their way into one of three groups:

1. Employers who sign up with CalSavers.

2. Employers who create an alternative retirement plan.

3. Employers who will potentially pay the noncompliance penalty.

Clearly, Group #3 will be naturally avoided, but due to the specific approach that CalSavers has taken (as explained below) Group #1 might also be something many employers will want to avoid.

Therefore, understanding which of the alternative programs is the right fit for a given employer will be the key resource a broker can deliver to clients and prospects that are formulating their compliance strategy.

Navigating CalSavers’ challenges

While CalSavers takes significant steps to make the employer sign up as easy as possible, there are aspects to how the CalSavers program works, both during installation and on an on-going basis, that will present major challenges to some businesses. First and foremost it must be remembered that CalSavers generally requires “auto-enrollment” of all W-2 employees age 18+, regardless of hours worked. This is exacerbated by the requirement that employers play a limited role in the operation of the program. CalSavers attempts to shield employers from federal retirement plan ERISA requirements and fiduciary responsibility — and as a consequence, employers are required to take a neutral role in CalSavers and are told to direct employee questions about the program to CalSavers. Importantly, employers are not even permitted to accept employee opt-out requests directly. Opt-out communications must be from the employee to CalSavers and then CalSavers communicates the employee’s decision to the employer via a secure website (in other words employers’ payroll services must integrate the most up-to-date data on the CalSavers website before calculation of each and every paycheck.)

Many employers will not be comfortable with the extra burdens this places on their payroll departments or the “triangular flow of information” (where employees have to call CalSavers and then CalSavers communicates with employers.) Employers who have the following traits

CalSavers and Franchise Tax Board (FTB) Enforcement Calendar

might be particularly concerned about directly joining CalSavers:

- Have high worker turnover and/or seasonal workers

- Pay workers based on highly variable hour counts from one pay-period to another

- Face employee communication challenges (perhaps with non-English-speaking workers, or those with low levels of education and/or literacy)

A reluctance to join CalSavers will prompt many employers to seek compliance via one of the alternative programs that CalSavers accepts as a substitute. Here are those alternative programs:

- 401(a) – Qualified Plan (including profit-sharing plans and defined benefit plans)

- 401(k) plans (including multiple employer plans or pooled employer plans)

- 403(a) – Qualified Annuity Plan or 403(b) Tax-Sheltered Annuity Plan

- 408(k) – Simplified Employee Pension (SEP) plans

- 408(p) – Savings Incentive Match Plan for Employees of Small Employers (SIMPLE) IRA Plan

- Payroll Deduction IRAs with Automatic Enrollment

Even if you are not a retirement plan expert, you probably already know that employers take on significant long-term responsibilities and operational costs whenever they set up a qualified retirement plan. Most of the plans above involve employer funding of some (or all) of the retirement plan contributions for employees. The cost for this might be much more than an employer is willing to spend to simply become CalSavers compliant. On top of the cost of direct contributions, there are “soft” costs that come with non-discriminatory employee enrollment and on-going communication of investment options. To make matters even more complicated, most retirement plans require ERISA plan documentation and compliance, annual audits and IRS Form 5500 filings.

Introducing a simpler way to comply

Many employers will simply want to know how to meet their compliance burden with the easiest and least expensive approach. To be more specific, employers will be seeking the option that:

- Allows the employer to directly communicate with each employee, without outside involvement

- Eliminates the need for any employer contribution to employee retirement accounts

- Avoids ERISA plan documentation and communication responsibilities

- Doesn’t require annual reporting (Form 5500) to the IRS

- Avoids placing fiduciary liabilities on employers

- Is as inexpensive as possible to set up and maintain

When the list of possible alternative plans is screened with the above bullet-points as a filter, the option that remains is the Payroll Deduction Individual Retirement Account With Automatic Enrollment (PDIRAWAE, for short). In fact, the CalSavers website’s proclaims that the CalSavers itself is just such a program.

This potential problem can be turned into a significant opportunity for those brokers who take the time to understand both CalSavers and the various alternatives employers can implement to be compliant.

If an employer is seeking the easiest and least expensive option to offer to their workers, the PDIRAWAE deserves a look. But there is a bit of a catch…while the concept of a payroll deduction IRA has been around since the 70’s, CalSavers adds the requirement that any employer that wants to use this type of program must incorporate the automatic enrollment feature. Exactly how an employer is supposed to incorporate automatic enrollment is left up to the employer to figure out. Since automatic enrollment was/is not contemplated by any of the IRS or DOL guidance documents, there is little help from that direction. Therefore, creating a PDIRAWAE can be a bit puzzling to most retirement plan professionals.

Because of that automatic enrollment feature, a PDIRAWAE will require the employer to provide each employee with some basic plan communication documents. Interested employers can either hire their own professional resource (law firm, CPA firm or retirement planning consultant) to help them assemble the needed documentation or they can check out a new website that brings the PDIRAWAE to the marketplace in one self-contained package. That website is www.ezsavings4u.com.

The EZSAVINGS4U* program was specifically created to address the concerns of employers who want the easiest alternative to achieve CalSavers compliance. (Author’s note: The EZSAVINGS4U program was specifically designed by me and two legal and employee benefit collegues with over a century of combined experience to meet the compliance needs of the CalSavers program. Just like any private party retirement program, it is not endorsed, sanctioned, approved, or in any way affiliated with the State of California, the California Treasurer’s Office, or the CalSavers Retirement Savings Board).

Visitors to the EZSAVINGS4U website can access over five hours of informative video content, designed to help private-sector employers make the right decision for their unique needs. If employers are interested in moving forward, they can fill out a simple form to request customized plan documents and receive a full PDIRAWAE operations manual.

Because EZSAVINGS4U is offered for a nominal one-time fee, some independent brokers have decided to pay for this program as a value-added service to their clients. A few growth oriented brokers are even seeking to turn prospects into clients (via a broker of record letter) in return for the broker’s help in securing the employer’s access to the EZSAVINGS4U solution.

While the concept of a payroll deduction IRA has been around since the 70’s, CalSavers adds the requirement that any employer that wants to use this type of program must incorporate the automatic enrollment feature.

Conclusion

To summarize, CalSavers is the law. California employers who don’t provide workers a retirement plan must soon figure out for themselves if participating in CalSavers directly or opting instead to install an alternative is best for their business.

You, an insurance broker who cares deeply for your clients and hopefully can now recognize the opportunity for potential growth of your practice, are well-advised to understand the nuances of the CalSavers mandate and the available alternatives.

About CalSavers

CalSavers wants more of California’s workers to save for retirement. By law, employers with as few as five employees on payroll must register into CalSavers by the appointed deadline or create their own alternative retirement savings program.

CalSavers:

- Is one of 13 State Sponsored Retirement programs that are fully operational or are in some stage of development.

- Has already been challenged in Federal Court and been upheld as legal. It is within California’s rights as a state to enforce on employers.

- Is funded by employee payroll deductions, without employer fees or contributions.

- Is administered by a private firm (ASCENSUS) and overseen by a public board (chaired by the California State Treasurer).

- Via employer payroll systems, employees are “auto-enrolled” into CalSavers after their first 30 days of employment.

- All W-2 employees over age 18, even if only working part-time, are to be auto-enrolled.

- Gives employees the opportunity to opt out or back in at any time.

- The default contribution is 5% of pretax wages.

- Employees can increase or decrease their contribution percentage at any time.

- By default, contributions are placed into a Roth IRA, but can be converted to Traditional IRA.

- CalSavers has default investment options for initial deposits, but as the employee’s balance grows, employees have expanding investment options within CalSavers.

- CalSavers promises employers freedom from ERISA and fiduciary responsibilities, but as a consequence, the employer must play a limited role in communication and administration.

- Employers must direct virtually all employee questions about the program to CalSavers.

- Employers cannot return to employees any CalSavers deposits (that must be handled directly by CalSavers.)

- Employers cannot accept any employee requests to opt out or make changes to the default contribution percentage (that must be handled directly by CalSavers.)

Readers are encouraged to visit www.calsavers.com to learn more.

ED MCCLEMENTS, JR., CLU, ChFC, is the president of McClements Insurance Services, and the creator of EZSAVINGS4U. He has 45 years of employee benefit experience, including the past 30 years serving the agricultural industry. At age 14, Ed was the youngest person ever granted an insurance license in California. Formerly, he served as the executive vice president of United Agricultural Benefit Trust, branch manager for one of California’s largest insurance brokerages, and president of the Agricultural Personnel Management Association.

ED MCCLEMENTS, JR., CLU, ChFC, is the president of McClements Insurance Services, and the creator of EZSAVINGS4U. He has 45 years of employee benefit experience, including the past 30 years serving the agricultural industry. At age 14, Ed was the youngest person ever granted an insurance license in California. Formerly, he served as the executive vice president of United Agricultural Benefit Trust, branch manager for one of California’s largest insurance brokerages, and president of the Agricultural Personnel Management Association.