Get better protection for your hard-earned commissions

By Phil Calhoun

In this article we compare carrier beneficiary agreements with a Commission Protection Plan. We will explain the beneficiary agreement generally offered by carriers, then explain the shortfalls of these agreements. Finally, we outline a projected financial comparison with a common buyout agreement and how the numbers work in the sale of commissions.

To begin with you need to know only a few carriers offer a beneficiary designation option to protect a broker’s hard-earned commissions. This designation has important limits as it only fits when a broker dies and only applies to individual & family plans (IFPs) and Medicare supplement lines of business. When a broker completes a carrier designation, the surviving family cannot sell these commissions.

We can stop with these limitations and just advise NOT to use a Beneficiary Designation, but we will continue and explain the math we use to compare the two options:

1) “Protect then Sell”

2) the Beneficiary Designation with a carrier.

Since it is obvious we do not consider designating commissions as a viable solution, we want to bolster this case and outline two main concerns for a broker working on planning for commission protection.

First, the sale of commissions takes full advantage of the “selling at the peak concept.” Commissions always drop when a broker slows down since the perception is they are semi-retired. The more lightly aligned clients are susceptible to move to a new broker who may offer more service and new plans to consider such as a MAPD option especially when a client year after year is paying high premiums for their supplement policy. When brokers in this later stage situation provide less service and support, some clients may look to find another broker. Also compounding this reduced service impact, is when the broker’s death occurs there is an automatic drop in the value of commissions. Without a licensed and certified successor ready to pursue a pre-planned client retention effort, retention drops and clients can leave. Secondly, commission retention going forward is important and a beneficiary (often a non-licensed friend or family member) is unable to do the job necessary to help clients. Relying on carriers to do this service work is a recipe for retention failure.

Risks of carrier support of clients

When using a family member or friend as the unlicensed beneficiary, the assumption is commission retention will work without great effort. However, since the carrier is now 100% responsible for all service and support for clients and carriers have the responsibility for all client retention including during open enrollment, the chance of failure increases. With clients seeking information and making plan changes, the impact can result in a rapidly declining retention effort.

Overall, the beneficiary designation places clients at risk for three key reasons:

- Open enrollment (PDP, other Med Supp plans, and even MAPD) requires personalized assistance. Shopping for the best coverage, comparing options, requires personalized attention to the client’s needs. Carriers will never provide options offered by competitive carriers. Even when contacted, most carriers will not be easily accessible compared to an active broker. And finally, the carriers are not advocates for clients and will fall far short of the support an active broker provides their clients. Relying on a carrier for client and commission retention will quickly lead to lost clients, especially in situations where clients must rely on a carrier’s 800 number for all servicing, combined with an inability to compare or enroll in plans with other carriers.

This approach to succession planning effectively eliminates retention management and will lead to a shorter than desired time period for funds getting paid to unlicensed beneficiaries. We anticipate that on average, more than 70% of clients will move to another carrier or brokers within 6 years. IFP and Medicare clients do shop plans often and are heavily marketed directly.

- Logistics are complex. When working with any carrier that offers a beneficiary designation option, the broker must place the request while alive and use the carrier’s formal process. Any request must be approved ahead of a life event so when the timing is last minute, which is often the case, mistakes can be made in an urgent, time sensitive situation. Carriers can have completion timelines which if missed will close the option for the designation. Staying current with carrier agreements is important as well since carriers can change the terms of the agreement over time. A review of carrier agreements shows carriers have the right to change their broker agreement to modify commission amounts and conditions of payment at any time. History shows carrier decisions of this type do change. Also accounting which includes clients and then monitoring carrier payments can take time and some expertise. In a traditional commission transfer between a seller and buyer the carriers rarely get this correct and both buyer and seller work together to proactively review carrier statements. A great deal of importance is placed on active client management each month.

While the beneficiary option is better than nothing, the best practice is to have a comprehensive plan for 100% commission protection and doing the work required to reach the highest possible retention.

- Final thoughts on beneficiary designation agreements. A key goal in commission protection is to pay loved ones out when retiring or after death. This is due to the fact commission protection planning uses a best practice approach that will create a much better solution. A $200,000 book of business could sell for two or three times yielding $400,000 to $600,000 with a viable successor. This result is compared to a beneficiary arrangement where a slow financial draw down happens as clients change plans and move to brokers who can help them. While the payout may last a couple years, the business will quickly vanish as clients experience poor service and go through the pressures of sales tactics with limited objective assistance.

Ask yourself if most of your clients will stay with the same carrier and on the same plan for the next several years. If the answer is a yes for 90% of your clients, the beneficiary designation could fit your needs.

Since carriers only include IFP and Medicare supplement plan commissions with a beneficiary designation option, our position is to seek a comprehensive, viable and modern commission protection solution for all of your Medicare commissions. A solid Commission Protection Plan with a purchase agreement included, can beat a carrier driven beneficiary designation process.

We do applaud the effort carriers have made to help brokers; this is one situation where it is best to compare your options.

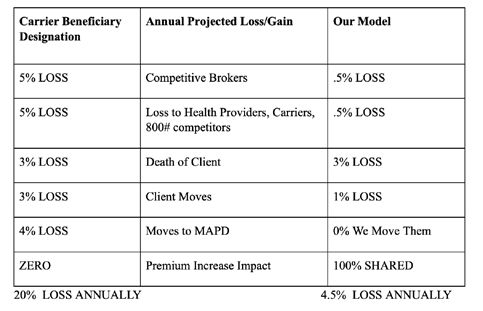

Chart Summary

A few carriers offer the option to get paid up to 70% of ONLY your Medicare supplement commissions with the carrier’s beneficiary designation option. The chart shows why this carrier option results in far reduced ability to protect a broker’s commissions. This results in much lower payments compared to a protection and sell option. The problem with the beneficiary designation option is the combined impact of:

- competition from brokers

- aggressive marketing from health care providers, other carriers and well-funded 800# agencies

- client-initiated moves

- when a Medicare supplement client moves to MAPD even with the same carrier

- carriers never pay more as premiums increase over time.

When an agency or a local independent broker provides commission protection and then purchases the commissions upon broker retirement, the ability to protect commission is far better. A broker can protect against competition with active service and support, service work not outsourced but provided internally. When a client moves, a broker can manage within the state and outside the state with multi state licensure, giving them the ability to move clients to new plans. Most brokers who purchase commissions include payment of all commission increases due to premium increases or plan changes during the payout period.

To demonstrate:

20% Annual Loss Over 5 Years:

REVENUE Year 1 Year 2 Year 3 Year 4 Year Five

$100,000 $80,000 $64,000 $51,890 $40,960 $32,768

4.5% Annual Loss Over 5 Years:

REVENUE Year 1 Year 2 Year 3 Year 4 Year Five

$100,000 $95,500 $91,200 $87,100 $83,180 $79,440

Summary

The carrier’s beneficiary designation option is projected to net less than half the amount in five years, compared with a broker/agency-based commission projection plan. When the active broker decides to retire and sell, the typical payout annually is 50% versus 70% for the carrier paid.

Assumptions: Based on $100,000 of commissions, annual losses after transferring all retention work via retirement to the carrier (800 number) is 20% annually and the cumulative impact over 5 years is a reduction of $66,000 lost commissions or 66% of the total $100,000 starting point/year. The total loss over five years with an active professional broker’s retention effort after the sale is 20% or $20,000.

We assume a five-year period as many payout periods cover 5 years. Retention rates are assumed. Your results could be higher or lower. Net paid to beneficiaries is no less with either option assuming the carrier continues to pay, and retention is at least 83% and payout remains at 70% of total commission.

Final point

Hold onto your commissions and use a Commission Protection agreement.

Select a viable successor broker who agrees to pay you upon your retirement and to pay your beneficiaries after your death. Payments in most cases will be the amount agreed upon with the buyout paid over a defined payout period. Often for Medicare supplement commissions this is 50% of collected commissions for six years. Retention will be higher than a carrier can manage, and most successors will agree to pay based on received commissions which include increases due to age rate increases.

Check out our website for information on

Commission Protection, Growing Commissions, and Selling Commissions. www.commission.solutions

To arrange a no obligation 15-minute coach session, “Click to Book Here”

or call 714-612-0306

Phil Calhoun is owner and publisher of California Broker Magazine. Phil also is a leader in coaching health insurance professionals. He is an active member of several insurance associations including the California Association of Health Insurance Professionals (CAHIP) and local chapters in Orange County, Los Angeles, San Diego and Inland Empire Health Insurance Professionals. He attends many state and local California chapter meetings.

Phil’s book, “The Health Broker’s Guide: To Protect Grow and Sell Commissions” is available free at www.healthbrokersguide.com.

He offers complementary 15-minute coaching sessions. To schedule a phone call “Click Here”

Contact:

714-664-0311