Long term care costs have been increasing faster that the rate of inflation for years, and COVID-19 exacerbated the increases in 2020

BY LOUIS H. BROWNSTONE

This is evidenced by the just released 2020 Genworth Financial annual Cost of Care Survey. Genworth contacted nearly 60,000 long term care providers nationwide to complete almost 15,000 surveys for nursing homes, assisted living facilities and home healthcare providers.

The manager of the Genworth survey, Gordon Saunders, said that providers “told us that the same factors responsible for the continuing increase in long term care costs in recent years were made even worse by the pandemic — a shortage of workers in the face of increasing demand for care, higher mandated minimum wages, higher recruiting and retention costs, and an increase in the cost of doing business, including regulatory, licensing and employee certification costs.”

In addition to these rising costs, staffs have had to meet all the challenges of caring for their clients with all the emotional stress that has resulted from COVID-19. Roughly 40% of all deaths in America from the pandemic have involved care facilities.

For the United States as a whole, the largest annual increase was in Assisted Living Facilities, where rates increased by 6.15% to an annual national median cost of $51,600 per year. The costs of Home Health Aides increased 4.35% to an annual median cost of $54,912 per year. The cost of a semi-private room in a Skilled Nursing Facility rose to $93,075, an increase of 3.24%, while the cost of a private room in a nursing home increased 3.57% to $105,850. Maybe the lower increases in nursing facilities was due to a relative lack of demand as the pandemic heightened the desire of people to stay at home whenever possible.

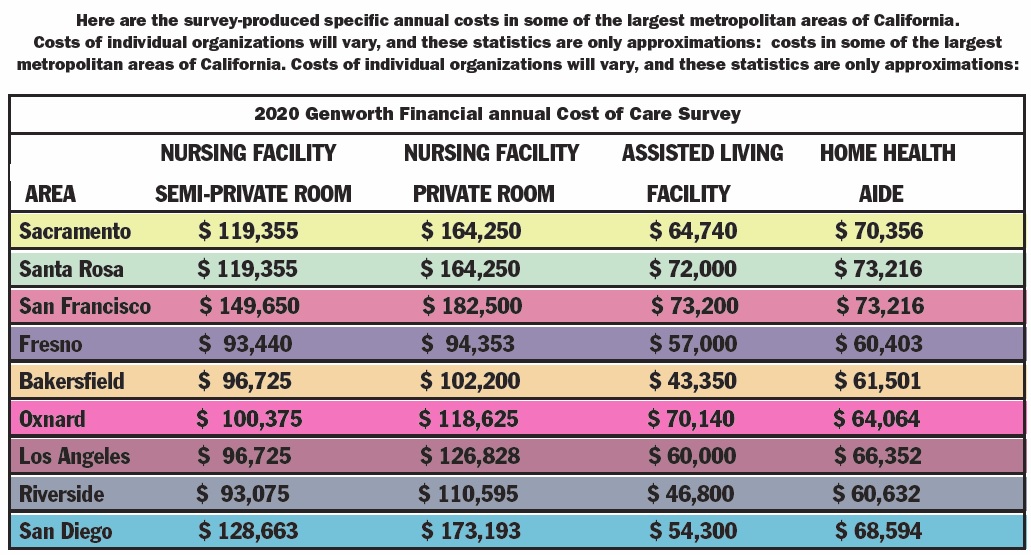

Looking at the state of California, the costs vary by region, but the median costs for the state are somewhat higher than the national medians. The largest annual increases were in Nursing Facilities. The cost of a semi-private room rose 5.56% to an annual cost of $110,960, while the cost of a private room rose 7.43% to $137,240. Assisted Living Facility cost rose 3.90% to an annual cost of $60,000, or $5,000 per month, and the cost of a Home Health Aide rose 3.57 % to an annual cost of $ 66,352.

The San Francisco Area contains the highest costs, but the Sacramento, Santa Rosa and San Diego Area costs are also higher than the state median costs. The exception is Assisted Living Facility costs in the San Diego Area, which are among the lowest in the state. The Los Angeles area costs are less than those of the other large metropolitan areas.

Here are the survey-produced specific annual costs in some of the largest metropolitan areas of California. Costs of individual organizations will vary, and these statistics are only approximations:

These sharp rises in costs over many years, including 2020, create some significant questions.

First, one would predict that the future rises in costs may well continue to be substantially greater than the general rate of inflation. The long term care “elephant in the room” could well become larger. How in the world are most people going to be able to protect themselves from future devastating long term care costs?

Second, one would question the adequacy of most long term care insurance policies which have been sold. I’m a believer that partial coverage can be very effective protection, but when is partial coverage so partial that it is no longer adequate to do the job for which it was intended? If the costs of care continue to increase at annual rates way above 3%, current policies sold may fall way behind in covering future costs.

Most policies that have been sold in California are way short of covering the current costs of nursing facilities or twenty-four hour per day home care. They may even only partially cover the costs of an assisted living facility or up to eight hour per day home health care. Even the default inflation rider, 3% compound inflation, may not cover the rising gap in coverage vs costs over twenty or thirty years.

Third, do hybrids or linked life insurance policy solutions cover this rising gap in coverage versus costs any better than traditional long-term care insurance? Many may not, with their relative lack of inflation riders and their 1%, 2% or 4% automatic pay-outs. Others without payout restrictions may invade most or all of the death benefit in a relatively short period of time.

The result is that we have a long way to go to solve “the elephant in the room,” and may well require a viable private-public partnership solution.

LOUIS H. BROWNSTONE is chairman of California Long Term Care Insurance Services, Inc., located in Burlingame. California Long Term Care is the largest independent specialist long term care insurance agency in California, and is broker for a group of high-producing long term care specialist agents. Brownstone is also very active in NAIFA, the National Association of Insurance and Financial Advisors.

LOUIS H. BROWNSTONE is chairman of California Long Term Care Insurance Services, Inc., located in Burlingame. California Long Term Care is the largest independent specialist long term care insurance agency in California, and is broker for a group of high-producing long term care specialist agents. Brownstone is also very active in NAIFA, the National Association of Insurance and Financial Advisors.